Nobody likes getting into a car accident. From the high-pitched screech of tires to the thunderous sound that comes when two cars slam together, the entire experience can jolt you to the core.

Even the smallest of crashes – a fender bender – can shatter your nerves for the rest of the day.

According to a U.S Census’s Motor Vehicle Accidents and Fatalities report, on average, there are 6 million car accidents in the United States. But how many of those accidents are really accidents?

Right now, as your eyes glide across the words in this article, someone is planning a staged accident. Seasoned swindlers – including unethical doctors and lawyers – have formed crime rings that bilk insurance companies out of billions of dollars each year through staged accidents.

Insurance companies are not the only ones getting ripped off. Consumers also pay the price of staged accidents by way of rising insurance premiums. What’s worse, staged accidents are just a lead-in to other forms of auto insurance fraud.

According to the National Insurance Crime Bureau (NICB), staged accidents set the stage for subsequent acts of fraud ranging from faked or exaggerated injuries to unnecessary or excessive medical treatment.

Take for example the case of Mikhail Zemlyansky, a Long Island man who is now serving 15 years in prison for masterminding the nation’s largest no-fault auto insurance scam. Prosecutors alleged that Zemlyansky and more than 30 others cheated auto insurers out of hundreds of millions of dollars and conned more than 300 victims, including the elderly, out of $17 million.

“The Zemlyansky case is a stellar example of how teamwork among the feds, NYPD, the National Insurance Crime Bureau and major insurers put one of the nation’s most-prolific automobile crime rings out of business,” says James Quiggle, director of communications at the Coalition Against Insurance Fraud.

Quiggle also emphasizes the importance of consumer awareness in helping to fight fraud rings.

MORE: What to Expect in Traffic School

“Alertness by consumers to see the warning signs of a staged crash in progress or at the scene of a crash can play a big role in combating large, organized rings that are elbowing into insurance fraud,” Quiggle says.

Fortunately, staged accidents are not difficult to spot and prevent. Even at the crash scene, there are telltale signs that can help investigators determine if it is an attempt at fraud.

Common types of staged car crashes:

Swoop and squat

You are driving along in traffic and without warning, a car pulls in front of you and intentionally hits the brakes causing a rear-end collision.

Drive down

You are attempting to merge into freeway traffic when a driver waves your car forward. You merge over and the driver deliberately crashes into your car, making it look like you are to blame for the accident.

Sideswipe

You are making a left turn from an intersection with dual left-turn lanes. You drift slightly into the other lane so the driver sideswipes you.

T-Bone

You come to a complete stop at an intersection and then cautiously proceed through when a driver slams into your vehicle and claims that you ran the stop sign.

Wave-in

You are driving in heavy traffic and want to switch lanes. A driver waves you in and then slams into the back of your car claiming that he or she never waved you in.

Start and stop

You are driving along in heavy traffic. The driver in front of you starts to accelerate and as you begin, the driver slams the brakes causing a rear-end collision.

Warning signs that you were involved in a staged accident:

- The damage to the vehicle is minimal but the driver and passengers all complain of back and neck pain.

- The driver of the other vehicle or a complete stranger who shows up shortly after the accident provides a referral to a repair shop, doctor and/or lawyer.

- A tow truck immediately pulls over and offers to tow you.

According to the Coalition Against Insurance Fraud, you can protect yourself against falling prey to accident scams by following a few tips:

- Never tailgate.

- Apply your brakes if you see traffic slowing ahead of you.

- Count the number of passengers in the car(s) you collided with and get their names, phone numbers and driver’s licenses.

- Take cell-phone pictures of the other car, the damage it received — and the passengers.

- Call the police to the scene. Get a police report with the officer’s name, even for minor damage.

- Get involved if you are a witness. Watch for the warning signs of a scam.

By Aaron Crowe

Online research is a smart way to evaluate a new car before buying, but it can’t replace getting the feel for a car with a test drive, auto experts say.More than one in 10 new car buyers skip the test drive, figuring the car is meant to get them from point A to point B and that a test drive isn’t needed, according to a recent study by Maritz Research.

The study found that 11.4 percent of car buyers didn’t test drive their car before buying it, though 52 percent found the test drive to be very influential in their decision to buy.

Drivers may assume that if they’re buying the same brand and model of car that they previously had, it isn’t worth test driving, says Chris Travell, vice president of strategic consulting for Maritz Research.

“This is unwise since the average American has been out of the car market for 6.5 years,” Travell says. “There have been huge advances in technology, vehicle design, ride and handling.

“The car the customer bought six or seven years ago is very different from the car they can buy” now.

For drivers who do test drive a new car before buying it, there’s much more to it than seeing how fast it accelerates when getting on the freeway, experts say. If shoppers really want to get a feel for a car before buying it, here are some things to check for in a test drive:

City driving vs. highway driving

Mileage varies by how the car is driven, and so does a driver’s experience in the car. See how it handles on city streets and on the highway. Does it have enough power on a freeway onramp to safely enter traffic? Is it comfortable at slow speeds?

Test the brakes and turning at different speeds.

Car comfort and ergonomics

Car comfort and ergonomics

Can you get in and out easily? It’s a basic question that all buyers should answer, says Cathy Nesbit of Harry Robinson, a Buick and GMC dealer in Fort Smith, Ark. The driver should be able to reach everything comfortably, be able to easily adjust their seat, and have a comfortable seat, Nesbit says.

Do you need three rows of climate control or is one up front enough? And don’t forget cup holders.

Ergonomics can also be a hindrance to driving if there are too many gadgets and things in the car to keep your eyes on, says Chuck Hawks, a professional driver coach. “How distracting is the interior of the car?”

Basics of automobiles

Along with good acceleration, check that the brakes feel good, it turns well, and you can see everything around you. Check for blind spots. How is the wind and road noise?

Check out the trunk and back seats

Open the trunk and make sure there’s enough room for what you plan to use it for, recommends Mike Rabkin, president of From Car to Finish. If the rear seats fold down, test them, and check how easy it is to open and close the trunk and all of the doors.

CHECK OUT: How to Know You’re Getting the Cheapest Car Insurance

If you have kids or other passengers, check that the back seats are roomy enough for them. Rabkin suggests putting the tallest rider in the back seat and putting the front seat all the way back to test for leg room.

Dashboard and under-the-hood technology

Have the salesperson show you how all of the technology works in the car. This can include hands-free, voice activation, Bluetooth, USB ports, navigation, back up cameras, lane departure signaling and other extras, Nesbit says. Also ask if the extras are included in the cost of the car and how much extra it will cost for you to buy them.

Driver’s view

Driver’s view

Checking for blind spots isn’t the only view to check. Move the driver’s seat and mirrors as much as possible to ensure you have a comfortable seating position, within easy reach of all relevant controls, and a safe line of sight through all windows and mirrors, Rabkin recommends.

Interior quietness

Turn the radio off and listen to how loud the interior is, both on local roads and highway speeds, Rabkin says. You might hear the wind, squeaks or loose trim, for example.

Take a long drive, or a long sit

Part of being comfortable in a car, as mentioned above, is how well the seat feels and ergonomics. But most test drives don’t allow enough time to see how a four-hour trip will feel and if the driver will still feel refreshed after a long drive, says Hawks, who recommends sitting in a car on the showroom floor for as long as you can.

“Instead of waiting in an office, just go sit in the carseat,” he says.

Also take a one-hour or longer test drive, provided the dealer’s OK with it and knows ahead of time how long you’ll be gone, Hawks says. If a dealer knows you’re serious about buying, an overnight swap of your car for theirs may be allowed, and will give you a better, longer test drive, he says.

ALSO: Alzheimer’s, Driving and How to Talk to Your Aging Parents

Getting a test drive shouldn’t be difficult — arranging one over the Internet or by phone will help ensure a salesperson is available for one — and it’s a step a car dealer should want a potential customer to take before buying.

The Maritz study found that nearly four out of 10 customers don’t take their most considered vehicle out for a test drive, leaving four people who might have bought the car if they had taken a test drive.

This story has been updated since its original June 11, 2013 publication.

You probably remember that moment as a teenager when you finally got your driver’s license. It’s the one time in your life that driving is truly thrilling. You climbed behind the wheel, that little plastic ID card in hand, ready to take on the world as a full-fledged driver. Or so you thought. At first, driving was fun but also a bit terrifying. You had to remember to turn on the blinker, what all the signs meant, and how to change lanes on a busy freeway without panicking.

Within just a few years, driving loses its luster. Mostly, it becomes just a function of your day. This may lead you to believe that you’ve mastered the motor vehicle, but is that really accurate? Are drivers really as good as they think they are behind the wheel?

We surveyed 2,022 people to find out just how perception and reality stacked up. Turns out, people really do believe they’re good drivers. But does the reality match their perception? Read on to find out.

Perception vs. Reality

Driving culture can vary by state. Some states are known for their big cities with awful commutes and road rage. Others are characterized by slow, laid-back drivers. But we wondered how each state ranked for safest drivers.

What were the top 20 states with the most self-reported “good” drivers, and how did they rank in terms of crash fatalities? We were interested in how states’ perceptions matched up with safety outcomes. It turns out that New Mexico, Maine, and Oregon have the most self-reported “good” drivers and rank 47th, 22nd, and 19th, in terms of crash fatalities. What do you think of the states with the best and worst drivers?

Thoughts on Driving Ability

Some say that generational differences impact driving ability. Perhaps it’s simply that older generations have been driving longer. Or maybe older generations have spent their lives driving with fewer distractions and with a different generational perspective on how to be safe. Either way, it’s interesting to compare how attitudes differ among generations.

We analyzed responses from Millennials, Generation X, and the Baby Boomers. Most respondents thought they were good drivers; however, it’s interesting to note that as their ages increased, so did their beliefs that they were excellent drivers. Regarding safety, all respondents felt that they were safe drivers, but Baby Boomers overwhelmingly proclaimed (by over 50%) that they were very safe drivers.

When Driving Becomes Dangerous

Have you ever been involved in an accident? The National Highway Traffic Safety Administration (NHTSA) reports that over 2 million people were injured in car accidents in 2014. With the shocking number of people who are seriously injured or die every year, car accidents are no small matter. Though safety features and better road designs help lessen those rates, the key to not getting hurt while driving is to focus on the road.

Our respondents were asked to report on their history of car accidents, which we then compared among the generations. Millennials had the lowest accident rate overall, but this generation also hasn’t been driving as long as the others. Interestingly, Generation X drivers have been in more accidents than Baby Boomers. Does that mean Baby Boomers are the safest drivers overall? We’ll leave that up to you to decide.

It’s All About the Skills

When it comes to some aspects of driving, it’s less about getting from point A to point B and more about your overall driving skills. Certain things are just trickier for some drivers than others, such as parallel parking. Additionally, things have changed in car-making trends throughout the last few decades, which leads to a decline in certain skills. Automakers are responding to these trends: for example, making fewer cars with manual transmissions.

We asked our survey participants to talk about their driving skills. The majority of Millennials said they couldn’t drive a stick shift (nearly 63%), while Baby Boomers were the biggest group (about 71%) to say they could drive a manual car. When it came to parallel parking, proficiency increased with age: About 56% of Millennials said they were very or moderately comfortable with this parking maneuver, while nearly 64% of Generation X and almost 73% of Baby Boomers reported the same confidence.

Testing Driving Knowledge

After finishing driver’s ed class, we all have to take the dreaded driving test. After finally passing, we move on to more important things, like actual driving. If you were to take a driving test today, would you be able to answer all the questions correctly?

We were curious to see if our participants could correctly respond to some of the common questions on written driving exams. Most chose the right answers. However, when it comes to who should go first at four-way stops, Millennials seemed the most confused.

Men vs. Women: Self-Perceptions

Ah, the age-old question of whether a man or a woman can do one thing better than the other. When it comes to driving, everyone has an opinion about the opposite sex. But what do they think of themselves?

The data from our respondents to two similar, yet differently worded, questions are intriguing. About 38% of men proclaimed they were excellent drivers, while only a little more than 25% of women felt the same way about themselves. However, when asked if they were safe drivers, men and women answered at similar rates across the board.

Gender and Accidents

Everyone seems to want to weigh in on gender and driving behaviors – from researchers to everyday people. Men are more likely to engage in high-risk driving behaviors, and road rage is an issue for them. Marketing researcher Brandon Gaille looked at road rage statistics and discovered that men are more likely to get angry while driving, which often leads to accidents.

We wondered how both genders would respond to our survey question about their accident rates. Interestingly enough, both reported an almost 50/50 split; over 54% of women had been the driver involved in an accident, and about 52% of men stated they had.

Gender and Driving Incidents

When it comes to gender and car accidents, statistics tell us that men get into far more accidents than women, especially when they are young. Men are more likely to engage in risky driving behaviors, like not wearing their seat belts and speeding. However, the greatest fatality rates for both genders occur during their first few and last few years of driving.

We searched through the Fatality Analysis Reporting System (FARS) database to find out just how much risk men take on when driving. With an overall car accident death rate of 10.59 per 100,000 people, men are 3.5 times more likely to die in car accidents than women. When it comes to speeding, drunk driving, and not wearing a seat belt or helmet, men are 4.3 to 5.2 times more likely to die from accidents involving these behaviors.

Gendered Driving Skills

Driving skills are an important part of being a good and safe driver. But how do those skills stack up when you look at them by gender? Stereotypes tell us that men are better at specific driving skills. But are they really?

We separated the responses to questions about parallel parking and manual transmission abilities by gender and looked at the results. Both genders seemed to think that they were moderately comfortable with parallel parking, with only a slight edge for men (35%) over women (31%). But far more men said that they felt very comfortable with their parallel parking skills at 33%, versus women’s response rate of less than 19%. When it comes to the ability to drive a manual transmission, over 61% of women said that they didn’t know how to drive a stick shift, whereas nearly 51% of men said that they could.

Men and Women Take the Driver’s Test

With the high-risk behaviors that men tend to engage in, at least while they are young, does this influence their results when taking a mock driver’s test? Granted, these questions are tricky; many of us tend to scratch our heads wondering if we actually know the right answer. Curious how men versus women would perform? So were we.

The responses to the questions may or may not surprise you. It turns out that men and women gave just about the same rates of right and wrong answers, with some pretty negligible differences. It looks like our driving patterns might be a bit different, but we have the same kinds of knowledge overall. Good or bad, we are all in it together.

Conclusion

For some, driving can symbolize the freedom of a fun weekend road trip. For others, it brings back traumatic memories of accidents and scary driving experiences. Most of us experience a mix of both. As research shows, our perceptions of our driving don’t always align with how we actually drive. With the advent of smartphones and their ability to distract drivers, we are at even more risk than ever before. Additionally, we know many of the driving rules that keep us safe, but some lack knowledge when it comes to who gets to go first at a stop sign.

Gender seems to be a serious issue regarding risk-taking. Young men tend to drive dangerously, which leads to serious injuries and death. When it comes to overall skills, however, it seems that men and women are about even.

Methodology

We surveyed 2,022 people on their driving skills and tested them with some basic driving questions. For our additional information on safety outcomes, we analyzed the FARS database for crash fatalities and specific driving behaviors like speeding, alcohol consumption, and seat belt usage.

Sources

https://www.washingtonpost.com/local/trafficandcommuting/little-old-lady-behind-the-wheel-not-the-baby-boomers/2015/06/17/8fa601b8-04b1-11e5-a428-c984eb077d4e_story.html

http://www.iihs.org/iihs/topics/t/distracted-driving/topicoverview

http://www-nrd.nhtsa.dot.gov/Pubs/812246.pdf

http://www.roadandtrack.com/car-culture/a6308/whats-really-killing-the-manual-transmisson/

http://www.iihs.org/iihs/topics/t/general-statistics/fatalityfacts/gender

http://www.ncbi.nlm.nih.gov/pmc/articles/PMC4117653/

https://healthfinder.gov/FindServices/SearchContext.aspx?topic=14522

https://www.researchgate.net/publication/288041152_Sex_and_Age_Differences_in_the_Endorsement_of_Sex_Stereotypes_Associated_with_Driving

http://journals.plos.org/plosone/article?id=10.1371/journal.pone.0150227

http://www.iihs.org/iihs/sr/statusreport/article/50/1/1

https://www.buzzfeed.com/justinabarca/can-you-actually-pass-a-driving-test?utm_term=.hq78aw2EX#.ce65zjn9x

http://brandongaille.com/21-startling-road-rage-facts-and-statistics/

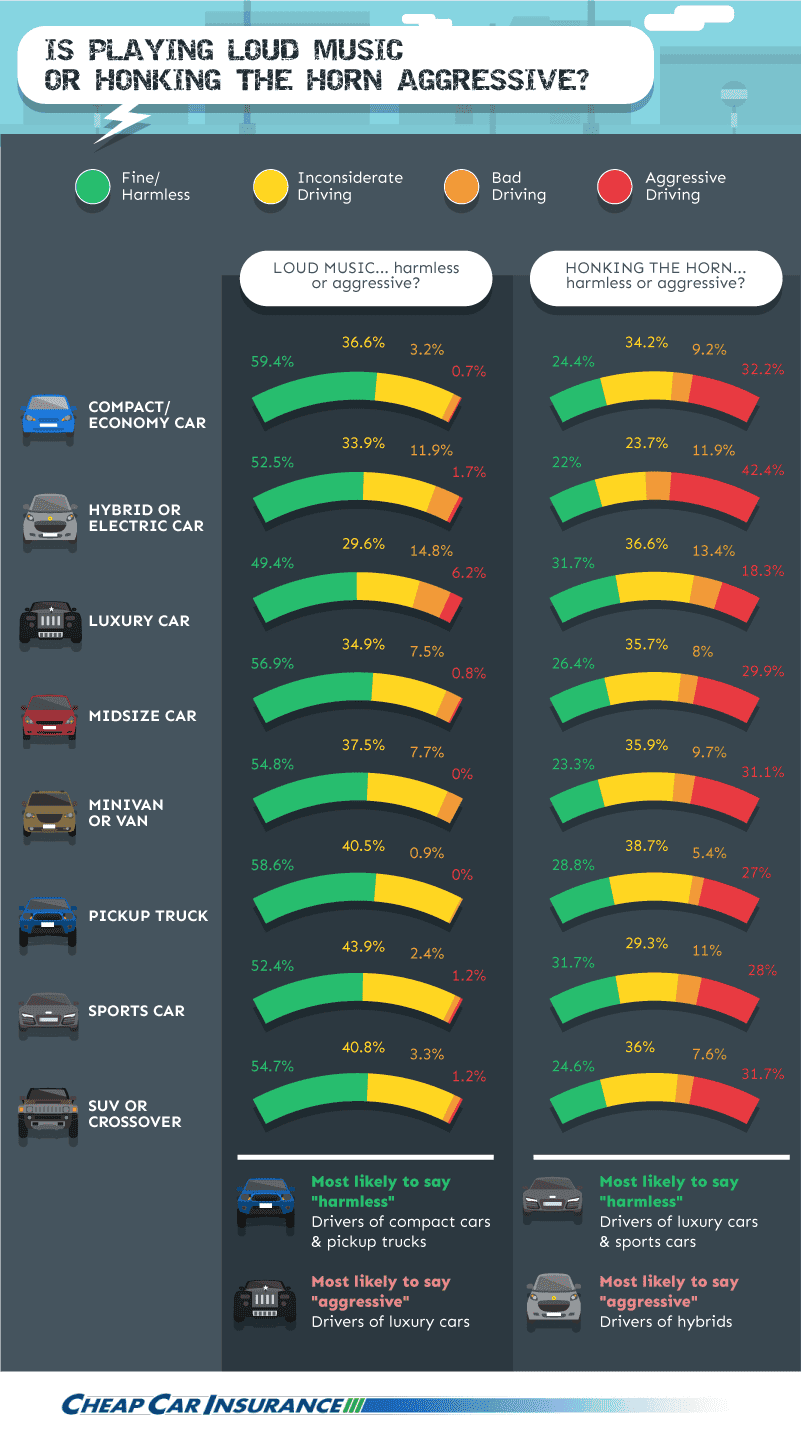

Obnoxious. Pushy. Combative. Whatever you call these drivers, you’ve surely encountered them on the road at some point or another. But what actions cross the line from simply rude to flat-out aggressive? Is one state’s aggressive driving simply another state’s norm? And how do opinions vary among different age groups, genders, and drivers of certain vehicles?

To get a handle on how Americans feel about aggressive drivers, we surveyed 2,000 drivers on the subject. They shared their feelings about everything from horn honking to hand gestures – and some of the results just might surprise you. Keep reading for the uncensored truth about anger and courtesy on the road.

What Is Aggressive Driving?

Just what does aggressive driving entail? We presented survey respondents with an array of behind-the-wheel behaviors and asked them to rank them on a scale of 0 (harmless) to 3 (aggressive), with inconsiderate and bad driving falling in the middle. The acts deemed most aggressive came with threats of physical harm: ramming a vehicle, trying to run a car off the road, wielding a weapon, and making sudden moves.

Running a red light, preventing a fellow driver from passing or merging, and making a rude hand gesture fell in the middle. Playing loud music was ranked least threatening of all, followed by driving slowly down the left lane, honking, and scowling at other drivers.

Bad Drivers in the Busiest States

No interstate rivalries come into play here: We asked drivers in the four most populous states to rank the skill levels of their own state’s drivers – and the results are in! Who’s the worst? Florida drivers get the lowest ratings, followed by Texas and California. On the other hand, New Yorkers take the cake when it comes to skillful driving.

Courteous Drivers in the Busiest States

When it comes to exhibiting kindness on the road, it turns out Southern gentility rules: Among the four most populous states, drivers from the Lone Star State awarded fellow Texans the highest scores for their courteous driving. However, New York drivers – honk! “Get out of the way, bud!” – were deemed the rudest. California and Florida fall in the middle of the polite-driver pack.

Vehicle Types and Aggressive Driving Opinions

Does the type of car someone drives affect his or her outlook on fellow drivers’ behavior? Drivers of pickup trucks and compact cars are the most likely to consider it harmless when fellow motorists blast music; luxury car drivers, on the other hand, are by far the aptest to find it aggressive. What about horn honking? Drivers of luxury vehicles and sports cars are likeliest to deem honking the horn harmless, while hybrid car drivers are the most likely to think it is aggressive.

People driving hybrids and sports cars are the most likely to rate flipping the bird or other rude hand gestures aggressive, while drivers of minivans were the most apt to find them harmless. As for tailgating, hybrid and sports car drivers are the likeliest to find the risky act harmless, while drivers of pickup trucks think following too closely is an aggressive act.

Rudeness While Driving in Private and Public

Everyone feels annoyed behind the wheel sometimes. But there’s a big difference between swearing under your breath and cursing loudly at another driver. Over 21 percent of our respondents admit they swear at other drivers daily – but only under their breath. Another 26.5 percent do so weekly, and over 21 percent hurl quiet profanities around once a month. Just over 12 percent say they’ve never been uncivil on the road.

On the other hand, only 1.6 percent swear loudly or make offensive hand gestures to other drivers every day. Just over 5 percent are publicly rude around once a week, while just under 9 percent lash out around once a month. However, nearly 54 percent say they’ve never cursed or flipped the bird at a fellow driver.

Car Color and Behind-the-Wheel Aggression

As marketers know, color is powerful: It can affect a person’s mood and even raise or lower blood pressure. But does the color of a person’s car affect how colorful their behavior is behind the wheel?

An assessment of personality based on car color by a color consultant and trend forecaster asserted that drivers of black cars are “powerful” and “elegant” – but our survey revealed that they are the most likely to honk their horn or chew out other drivers. “Outgoing” and “dynamic,” red car owners ranked second for likeliness to get angry, followed by otherwise “calm” or “confident” drivers of blue cars.

Interestingly, our survey revealed that drivers of yellow cars (who tend to be “joyful,” according to the color expert) are by far the least likely to behave angrily toward other drivers.

Aggressive Driving Across Generations

People from each generation have unique traits and outlooks – including their views on aggressive driving. Baby Boomers (ages 52 to 70) are by far most likely to deem loud music aggressive and inconsiderate, while older millennials (ages 25 to 34) are aptest to find it harmless.

Interestingly, younger millennials (ages 18 to 24) are the most likely to view honking as aggressive, while Generation Xers (ages 35-51) are least likely to consider it aggressive.

When it comes to rude hand gestures, again younger millennials are the most likely to feel that flipping the bird is an act of aggression. Baby Boomers are much less likely than every other generation to think it’s harmless, but they do not feel quite as threatened by the gesture.

Courtesy and Rudeness on the Road

Finally, we asked respondents to open up about the behavior they see on the road every day. The verdict? Just under one-fifth of people encounter offensive drivers (who refuse to let them change lanes or merge) virtually every day. Another 36.5 percent run into the issue at least once a week.

As for courteous drivers who slow to let people change lanes or merge? Just over 16 percent experience this daily, while nearly 47 percent encounter kindness on the road once a week. It’s clear in this situation at least, that courtesy rules.

Dealing With Aggressive Drivers

As our survey reveals, definitions of harmless and aggressive driving can vary widely. Among factors that might color our opinions? Location, age, gender – and perhaps even the type and color of our own cars!

You can model courteous behavior on the road, but you can’t change other drivers’ behavior – however, you’re in charge of how you respond. If you encounter a driver who is behaving aggressively, try to avoid them at all costs. Don’t respond to gestures or even look at them. If the situation escalates, call 9-1-1 to provide a vehicle description and travel location.

Your behavior (and responses to bad behavior) can go a long way toward making the road a safer place for everyone.

Methodology

We surveyed 2,089 drivers in the U.S. between May 12 and May 15, 2016. Respondents were between the ages of 18 and 75 and came from all 50 states, plus the District of Columbia. They were 47.5% female and 52.5% male.

Sources

http://www.huffingtonpost.com/2011/11/27/how-color-affects-our-moo_n_1114790.html

http://www.today.com/home/blue-red-or-silver-find-out-what-your-car-color-t81381

https://www.dot.nd.gov/divisions/safety/streetskills/aggressivedrivers.htm

Fair Use

If you’re interested in using the images from this project, please feel free to do so. We simply ask that you attribute CheapCarInsurance.net for the content, and provide a link back to this page, so your readers can learn more about our work.

By Aaron Crowe

Can’t get your car’s Bluetooth system to sync with your phone? Does the car’s navigation system misinterpret your commands and not get you where you need to go? You’re not alone.

Can’t get your car’s Bluetooth system to sync with your phone? Does the car’s navigation system misinterpret your commands and not get you where you need to go? You’re not alone.

A recent study by J.D. Power and Associates found that 20 percent of all customer-reported problems on vehicle reliability were for problems with infotainment, navigation and in-vehicle communication systems. Tech is the most problematic area on most vehicles and is causing the industry’s 3 percent year-over-year decline in vehicle dependability, according to the 2016 U.S. Vehicle Dependability Study.

Complaints about technology were the top concern in this year’s study, up from the third most last year and fifth in 2014.

Getting technology to work correctly can be frustrating, as anyone who has set up a Wi-Fi system at home knows. But not having it work in your car — where entertainment, navigation and other systems can cost thousands of dollars extra from the dealer — can be especially frustrating.

And the car tech problems don’t go way with time. The study found that customers reported tech woes within the first 90 days of ownership, and that the problems were still bothering them three years later.

Bluetooth pairing and connectivity, along with built-in voice recognition systems misinterpreting commands, were the most reported problems. Navigation systems that are difficult to use or inaccurate are among the 10 most frequently reported problems.

“Most consumers these days expect a car to have Bluetooth,” which is standard in most vehicles, says Barb Tate, national fleet manager at a GM dealer in Toronto.

The voice navigation systems and touch displays in GM vehicles work well if a driver is trained well in how to use it, Tate says. The display looks like an iPad, she says, and customers best learn how to use it if a salesperson lets them push the buttons instead of the salesperson pushing them. Different accents and intonations can affect how voice-activated systems work, Tate says.

“A lot of people don’t have the patience to let the technology do what it can do,” Tate says.

Integrated Bluetooth for phone calls and music streaming was a key feature that Nenad Cuk, 27, wanted when he paid about $2,500 more for a 2013 Hyundai Sonata Limited with extra tech features. Cuk, a marketing manager in Salt Lake City, Utah, said he got the streaming and pairing to work, but giving voice instructions to it doesn’t work so well.

“The one thing I am not happy about though is the hands-free talking function, because I have been told that I sound muffled or far away,” he says. “This makes sense as the microphone is fixed, but apparently it is fixed on a location that makes it hard for even me to reach. So sometimes I find myself taking the call into my hands, while driving, just so the other person can hear me better.”

Cuk also doesn’t use the car’s GPS often, and instead uses a map app on his phone. That may be the easiest go-around for drivers.

Paul Ritterbush, 29, of Berkeley, California, says the Bluetooth on his 2013 Ford Edge works great and links with his phone so calls come over the car’s speakers. Ritterbush found that a map app on his phone is more accurate and easier to use than the navigation system in his car.

These tech problems, which consumers may think should be simple to solve, don’t instill confidence in more complex technology such as autonomous cars that drive themselves.

“Right now, if consumers can’t rely on their vehicle to connect to their smartphone, or have faith that their navigation system will route them to their destination, they’re certainly not yet ready to trust that autonomous technology will keep their vehicle out of the ditch,” Renee Stephens, vice president of U.S. automotive at J.D. Power, said in a statement.

![]()

![]()

You’re driving home from work one evening and suddenly you see it: a police car hiding behind an overgrown tree. Panicked, you look down at your speedometer and realize you were driving well over the speed limit. Will you get away scot-free or be chased down by flashing lights?

If the latter occurs, you’re not alone. In the U.S., around 41 million people receive speeding tickets each year, which translates into around 112,000 per day. To find out more about speed trap trends across the nation, we analyzed 15 years’ worth of data from The National Speed Trap Exchange – a site run by the National Motorist Association that allows users to post information about speed traps and allows other users to vote on the credibility of the reports.

Do some states and cities have more speed traps than others? Where do motorists most frequently report seeing police cars hide? We also created an interactive feature so you can discover the most common cities for speed traps in your state. Read on to get the details.

Interactive: Cities Near You With the Most Speed Traps

Select your state from the drop-down menu to see which cities in your area are prone to numerous speed traps.

States With the Most and Fewest Speed Traps

![]()

![]()

A glance at the map reveals that some states rely on speed traps more than others. Several states in the Midwest and West fall on the low end, numerous states scattered across the country have slightly more, and one state accelerates to the top of the list: Vermont. With 52 speed traps per 100,000 residents, the Green Mountain State has over five times more than last-place Alaska.

In an effort to reduce speed-related fatalities, Vermont has been involved in state-specific and regional crackdown initiatives. One stretch of I-89 in Vermont is particularly notorious for speed traps: An officer parked under a canopy of trees has stopped numerous drivers for excessive speeding, defined as traveling 95 mph or more. New Hampshire, Michigan, Delaware, and Oklahoma all make the top 10 list for speed trap prevalence.

On the other hand, Alaska averages fewer than 10 speed traps per 100,000 people. A recent study revealed that the police force in Anchorage – the state’s biggest city – is understaffed. Speed traps in North Dakota, South Dakota, and Montana are also scarcer than average. Strikingly, these three states also rank in the top 10 in the nation for rate of car crash fatalities. Nationwide, speed ranks as a factor in just over a quarter of traffic deaths.

Worst Cities for Speed Traps

![]()

![]()

Even if your state isn’t crawling with speed traps, you may live near a city that’s notorious for them. Cities located in Florida, Michigan, Texas, Colorado, Pennsylvania, and Ohio all made the top 10. Sarasota, FL, had the most speed traps of all, with an average of 140 traps per 100,000 residents. Dearborn Heights, MI, took second place, and Coppell, TX, came in third. Even the No. 20 city St. Clair Shores, MI, had a surprising 78 speed traps per 100,000 residents. If you plan to visit to any of these cities, keep an eye on your speedometer – or better yet, set your cruise control.

Common Police Hiding Spots Reported by Motorists

![]()

![]()

When you think about speed traps, what do you envision? We analyzed keywords within speed trap data reported by motorists to determine the likelihood of speed trap locations. The most common phrase? “Side of the road” had 133 more mentions than the next-most-common term. Based on this analysis, other common locations for speed traps include at the bottom of a hill, at the top of a hill, in a parking lot, in a median, and on the side of the street.

Most Common Words and Terms Related to Speed Traps

![]()

![]()

We also analyzed phrases that motorists used when reporting speed trap information and created a word cloud to demonstrate their frequency. The larger the word is, the more prominently it was used. As you can see, drivers chat about location of speed traps (“parking lot”), reasons behind certain locations (“limit drops”), and even specific types of law enforcement (from “motorcycle cops” to “county sheriff”).

Top Intersections and Roads for Speed Traps

![]()

![]()

Speed traps aren’t located everywhere within a city – instead, they are strategically located in certain spots. We analyzed user-reported data (focusing on information deemed credible by other users) to uncover the spots where motorists have reported seeing speed traps the most. The chart above reveals the top spots in the U.S where you may be likely to encounter a speed trap.

Conclusion

You may live in an area where speed traps are common – or perhaps these stakeouts are not even on your radar. Either way, odds are you will drive by one at some point. As our report reveals, many states and cities across the nation are home to either drastically more or fewer than average.

There’s no doubt speed traps are controversial – although law enforcement maintain that the goal of speed traps is to increase safety, opponents assert that they are simply one more way for states and municipalities to generate funds. Some motorists even believe that police officers must meet ticket quotas or that they keep a cut of speeding tickets they issue (both are false). Websites and apps have sprung up to alert drivers to watch for them.

The truth? According to the National Highway Transportation Administration, 3 in 10 drivers are speeders. And in 2014, over half of speeding-related fatalities occurred on roads with speed limits under 55 mph. Your best bet to thwart speed traps is common sense: Don’t speed. Motorists’ top reasons for putting the pedal to the metal are that they’re late, they have an emergency or illness, or they weren’t paying attention. However, one fact rings true: No reason is important enough to risk your life or the lives of others on the road.

Methodology

We analyzed 15 years of driver-reported National Speed Trap Exchange data and determined viable speed traps by including only those speed traps that had more “yes” votes than “no” in order to ensure that we were not including any speed traps that were deemed “not a speed trap” by the NSTE community. For the “Most Driver-Confirmed Speed Traps Per State,” we pulled the speed trap locations with the most “yes” votes from our data that we were able to effectively geotag that had at least 25 “yes” votes and fewer than five “no” votes.

Sources

http://www.statisticbrain.com/driving-citation-statistics/

http://www.courant.com/news/connecticut/hc-windsor-highway-safety-0505-20150504-story.html

http://digital.vpr.net/post/one-stretch-i-89-excessive-speed-hotspot#stream/0

http://www.adn.com/article/20160317/anchorage-still-needs-dozens-new-officers-ideal-police-force-study-says

http://www.iihs.org/iihs/topics/t/general-statistics/fatalityfacts/overview-of-fatality-facts

http://business.time.com/2013/09/02/end-of-the-road-for-speed-traps/

http://www.cnn.com/2015/02/08/opinion/navarrette-waze-speed-traps/

http://www.wcax.com/story/18951854/drivers-caught-in-vermonts-new-speed-trap

http://www.nhtsa.gov/nhtsa/Safety1nNum3ers/august2015/S1N_Aug15_Speeding_2.html

Fair Use

Feel free to reuse any of the assets found in this project. When doing so, we ask that you please link back to Cheap Car Insurance and this page to give your readers a chance to explore our full report and the data behind it.

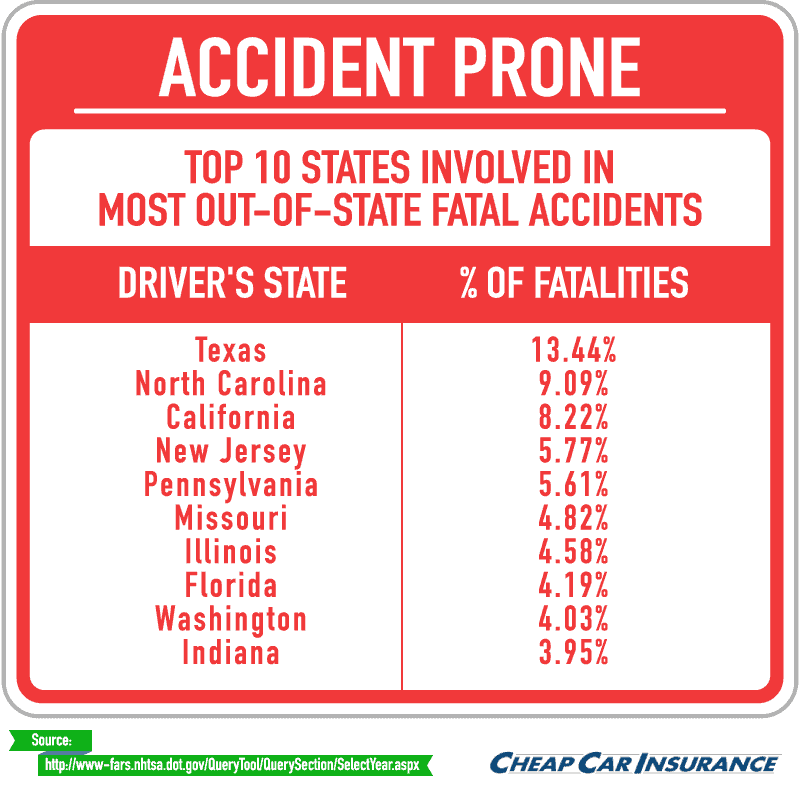

In 2014, 32,675 people died in motor vehicle crashes in the U.S. – and it appears that rate is only increasing. Every time you get behind the wheel, you have the potential to affect the lives of everyone else on the road. That’s why it’s vital to be the best driver possible. We’ve all heard the clichés about the skill levels of certain drivers, whether based on gender, race, or age. But in terms of these potentially offensive stereotypes, how much of the hype is even true?

To separate fact from fiction when it comes to accident-prone drivers, we gathered information from the National Highway Traffic Safety Administration’s Fatality Analysis Reporting System (FARS). How do the driving behaviors of people of different genders, races, and ages compare in terms of involvement in deadly accidents? And which states are home to the riskiest drivers? Keep reading to get the facts.

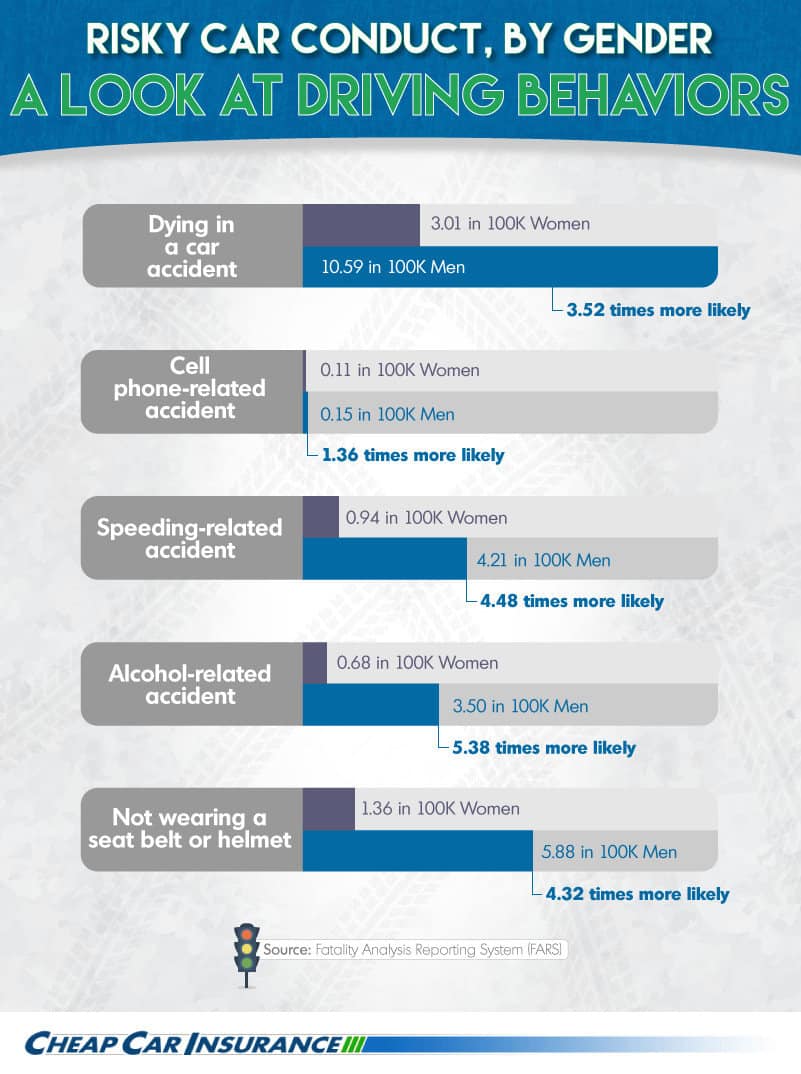

Risky Driving Behavior by Gender

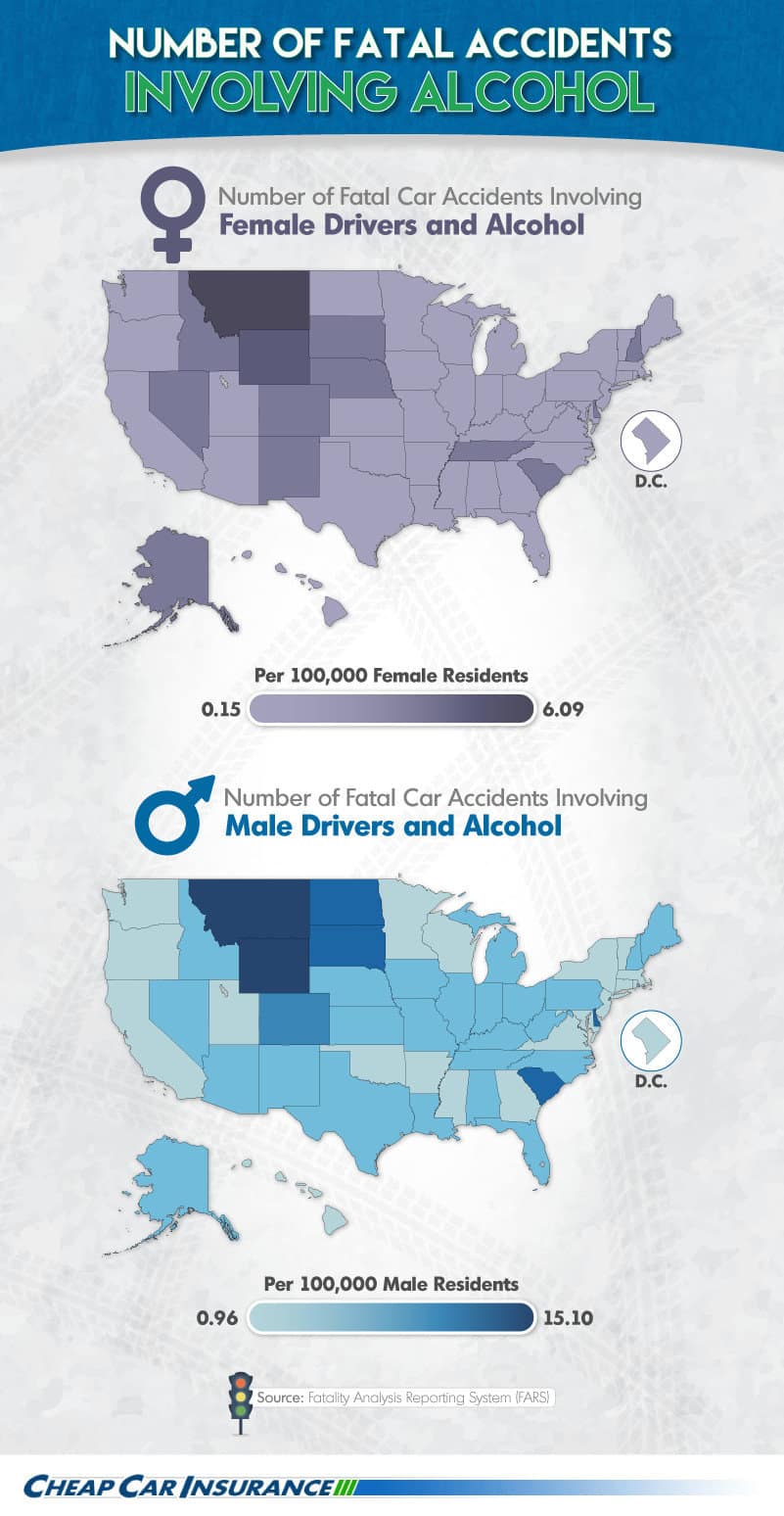

Have you ever heard someone crack a joke about women drivers? The above graphic reveals some telling facts that contradict this often-heard critique: Men are more than five times likelier to get in an alcohol-related accident, almost 4.5 times more apt to get in a speeding-related accident, and nearly 1.4 times likelier to get in a cellphone-related accident. Men are also more than 4.3 times likelier to forgo safety measures (seat belts in a car and helmets on a motorcycle). The result of this risky behavior? Men are more than 3.5 times likelier than women to die in a motor vehicle accident.

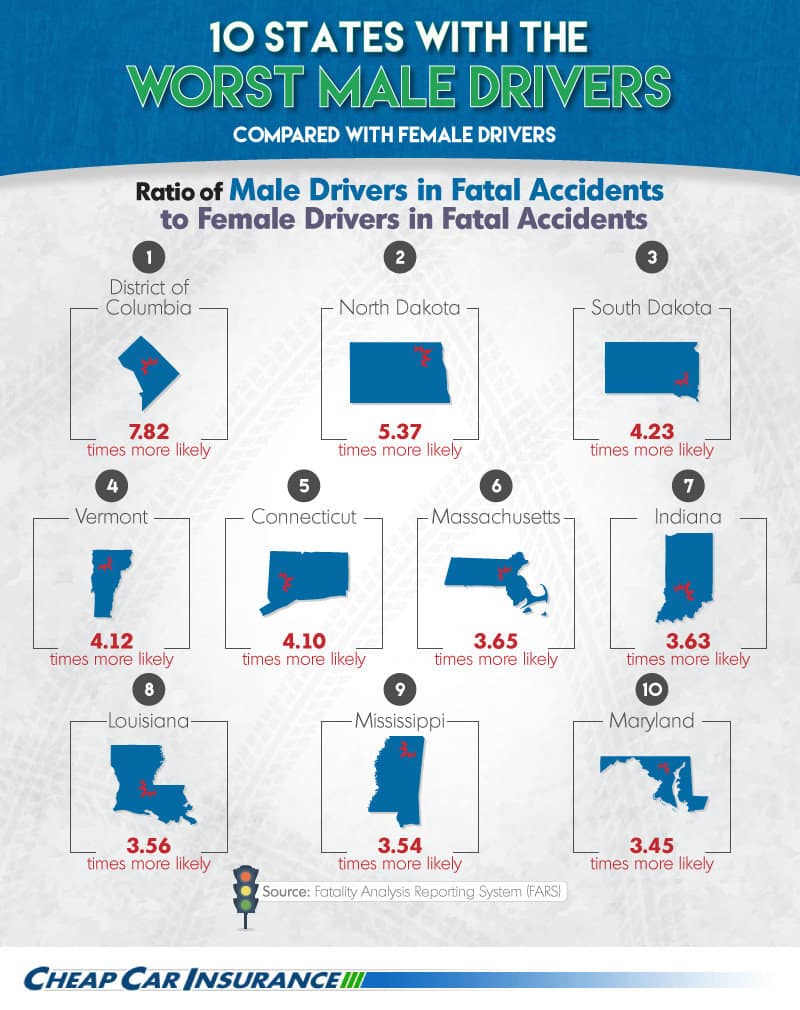

Risky Male Drivers by State

Overall, men are more likely than women to be involved in fatal accidents – and in some states, the difference is staggering. In Washington, D.C., male drivers are nearly eight times more apt to get in a fatal crash than female drivers. Additionally, men are over five times likelier to get in a deadly accident in second-place North Dakota and over four times likelier in South Dakota, Vermont, and Connecticut.

Accident-Prone States by Gender

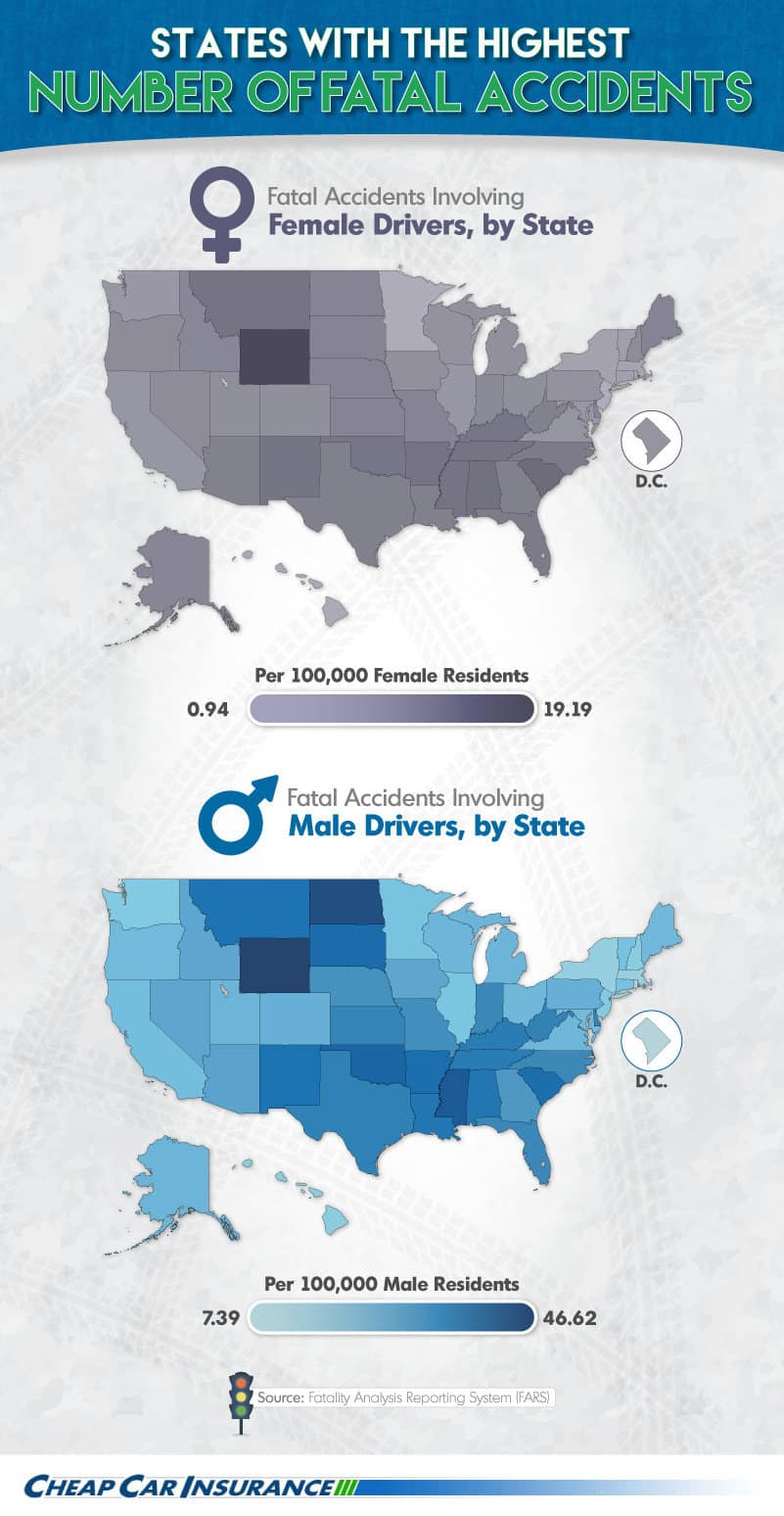

Fatal accidents can occur across the country, but the states in the graphic above see more than their fair share. Wyoming tops the charts for deadly accidents involving men and women: More than 46 per every 100,000 male residents are involved in fatal crashes, and over 19 per every 100,000 female residents are. Why? Its low population contributes to a high “per 100,000” rate, long distances can make it difficult for accident victims to receive timely medical attention, and officials report that many Wyoming drivers don’t use seat belts.

South Dakota takes second place for crashes involving women as well as fifth place for accidents involving men. North Dakota, Mississippi, and Oklahoma also make the top 5 for men, while Alabama, Montana, and Tennessee round out the top 5 for women.

Mapping Fatal Accidents by Gender

Comparing the maps of the highest number of fatal accidents involving either men or women paints an interesting picture. Overall, men are involved in many more deadly accidents than women. Some states show similarities – Wyoming is the top state for both genders, although men get in over twice as many fatal crashes. However, in North Dakota, the second-place state for male drivers, men average nearly 44 fatal accidents per 100,000 male residents, while women average only eight per 100,000 female residents. South Carolina takes second place for women, with almost 13 deadly crashes on average. On the other end of the spectrum, men in Washington, D.C., average just over seven deadly accidents, while women are involved in fewer than one.

Mapping Alcohol-Related Fatal Accidents

The map above focuses on fatal accidents that involve alcohol consumption. For both genders, Montana is the top state for these types of crashes: Men average over 15, while women get in just over six. Wyoming comes in second, with just over four accidents for women and nearly 12.5 for men. As for states with the fewest alcohol-related deadly crashes, New York saw fewer than one for men and Minnesota saw fewer than 0.2 involving women.

Mapping Speeding-Related Fatal Accidents

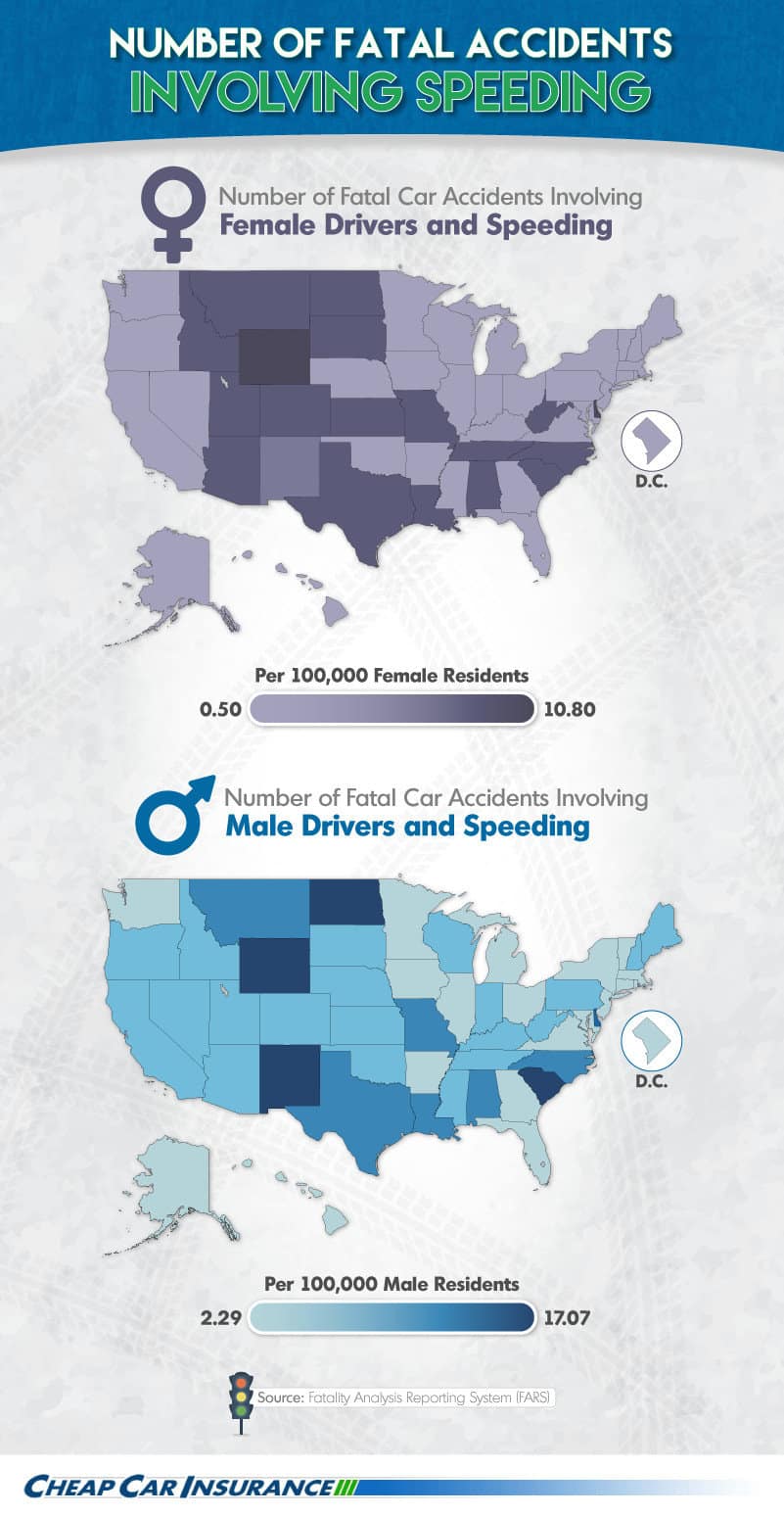

The above map zooms in on deadly accidents that involve speeding. Delaware is the No. 1 state for speeding-related fatal accidents that involved women, with almost 11 per 100,000 residents. Wyoming takes second place, with almost 10. When it comes to men and speeding, North Dakota claims the top spot with 17 accidents, followed by Wyoming (16) and New Mexico (almost 14.5). On the other hand, Massachusetts saw the fewest accidents for women, while Virginia had the fewest involving men.

Women’s Fatal Accidents by Race

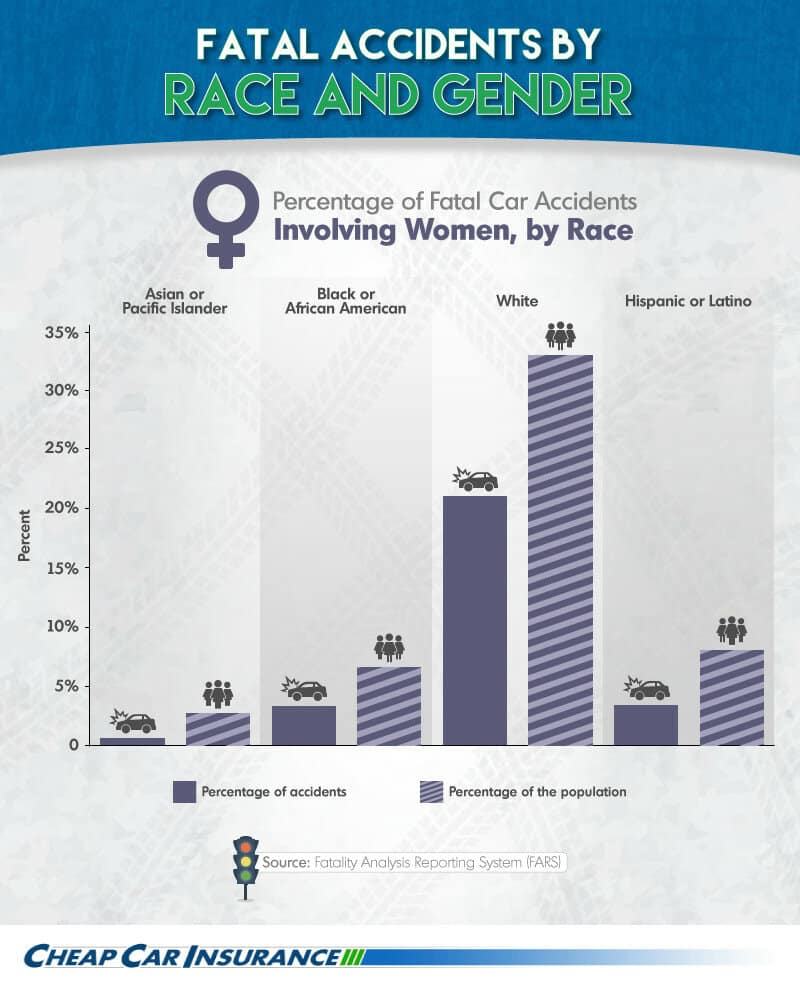

The graphic above provides a racial breakdown of women who are involved in deadly accidents. It appears that the stereotypes about certain minority drivers do not ring true. Asian/Pacific Islander women are involved in the lowest percentage of deadly accidents in proportion to their representative population. Proportionally, white women are involved in the highest percentage of fatal crashes, followed by black/African American women and then Hispanic/Latino women.

Men’s Fatal Accidents by Race

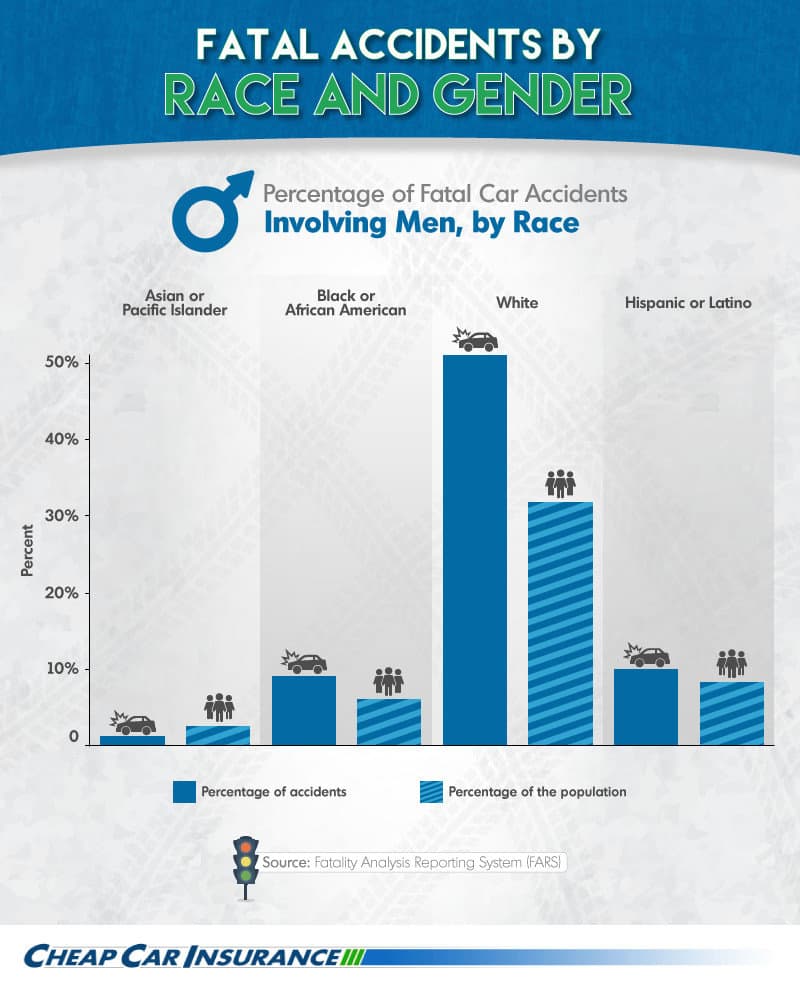

Breaking down the races of men involved in fatal accidents (based on each group’s population proportion) reveals a similar snapshot to the involvement of women: White men are involved in a much higher percentage of fatal crashes than any other group. Black/African American men come in second, followed closely by Hispanic/Latino men. Again, Asian/Pacific Islander drivers show the lowest involvement.

Driving Behaviors by Race

Conclusion

Driving is serious business – and it turns out that stereotypes about certain drivers are unfounded and certainly nothing to joke about. Our research offers a surprising glimpse of drivers’ involvements in fatal accidents broken down by gender and race.

Across the country, men are involved in more fatal crashes than women. Male drivers not only typically drive more miles, but they also tend to engage in risky behavior more frequently. Unfortunately taking certain risks can spell the difference between life and death – so it’s vital to obey road rules, utilize safety features such as seat belts and helmets, and never drive while distracted or under the influence of alcohol.

Methodology

The Fatality Analysis Reporting System (FARS) classifies a deadly crash as one in which a vehicle’s motion causes a fatality. We downloaded FARS 2014 raw data rather than using the querying tool, as it contains a wider set of criteria for driving behaviors such as speeding, the presence or use of alcohol, and cellphone use. The data pulled in this analysis will vary from the data pulled using similar variables in the querying tool due to the differences in criteria mentioned above. We collected information for fatal car accidents that occurred in 2014 and conducted the analysis in STATA using the “person,” “vehicle,” and “violation” files. We recoded “sex” in STATA so that our new variable only included “male” and “female”; it ignored records for “not reported” and “unknown.” For information on drivers, we looked at only “seat_position 11,” or the driver’s seat. The variables used for driving behaviors were: “mviolatn” (violations charged), “mdrdstrd” (driver distracted by), and “rest_use” (restraint system/helmet use). They were recoded as follows:

Drinking = 1 (yes, drinking was involved) if mviolatn = 11, 12, 13, 14, 15, 16, 19

Speeding = 1 (yes, speeding was involved) if mviolatn = 21, 22, 23, 24, 25, 26, 27

Cellphone = 1 (yes, cellphone use was involved) if mdrdstrd = 05, 06, 15

Seatbelt = 1 (no, no seatbelt or helmet was worn) if rest_use = 07

Variables concerning race were recoded as follows:

White = 1 if race = 01

Black = 1 if race = 02

Asian = 1 if race = 04, 05, 07, 18, 28, 48, 68

Hisp_rec = 1 if Hispanic = 01, 02, 03, 04, 05, 06

More information on the variables used can be found in the FARS User Guide 2014.

For our per capita calculations, we used Census 2010 data and for the “more likely to” calculations, we divided the male per capita calculations by the female per capita calculations, excluding instances that did not report the gender of the driver.

Sources

- http://www.nhtsa.gov/About+NHTSA/Press+Releases/2015/2014-traffic-deaths-drop-but-2015-trending-higher

- http://www-nrd.nhtsa.dot.gov/Pubs/812240.pdf

- http://www.wyomingnews.com/news/fatal-crashes-increase-in/article_385859e9-9f49-5b0f-9d86-72f0dea20310.html

- http://www.iihs.org/iihs/topics/t/general-statistics/fatalityfacts/gender

- ftp://ftp.nhtsa.dot.gov/fars/2014/DBF/

- ftp://ftp.nhtsa.dot.gov/fars/FARS-DOC/USERGUIDE-2014.pdf

Fair Use

Feel free to share the images found on this page freely. When doing so, please attribute the authors by providing a link back to this page, so your readers can learn more about this project and the related research.

By Craig Guillot

Americans with low credit scores are falling behind on car loans at a rapid pace.

Americans with low credit scores are falling behind on car loans at a rapid pace.

Fitch Ratings reported in March the number of subprime auto borrowers whose payments were more than 60 days late reached 5.16 percent — the highest rate in 20 years.

As more people are defaulting, the average car loan is increasing, too. According to Experian Automotive, the average new-car loan in the U.S. reached an all-time high of $29,551 at the end of 2015, and the average monthly payment was near $500.

If you’re falling behind or struggling to make your car payments, acting fast can help you save money, avoid hassle and maybe let you keep your car, too.

Contact your lender

Automotive expert Lauren Fix, also known as The Car Coach, says calling your lender is the first thing to do because “no financial institution wants you to default.” Repossession is often the least profitable option for a lender, she says. The lender has to cover the cost to repossess the car and then sell it at auction for less than market value.

“They would rather have you call than to not pay and totally ignore them,” says Fix.

Lenders have their own guidelines and regulations, but consumers may avoid repossession “if they’re acting in good faith,” says Steven Raj, vice president of Park State Bank in Duluth, Minnesota. “There are options. Full communication between the borrower and the lender is the first step.”

Options your lender can offer

One common option for people behind on car payments is a loan extension, Raj says. The lender can waive a few payments and then add them onto the back of the loan. The loan will still accrue interest, but a few months without payments can allow the borrower to catch up during a temporary financial strain. Lenders can also move the payment due date or offer refinancing.

Refinance

David Weliver, millennial financial expert and founder of MoneyUnder30.com, says you could refinance if you have good credit and haven’t fallen too far behind on payments. “Refinancing could make sense if the car is only a few years old, your existing loan has a high interest rate and your credit has improved since you bought the car,” says Weliver.

Landing a lower interest rate and extending the terms can significantly reduce your monthly payments.

Example: You’re in the third year of a five-year, $15,000 loan. Your interest rate is a steep 11 percent, and your payments are $326.14 per month. Refinancing that same balance for another five years at 3 percent (if you have good credit) would bring the payments down to $269.53 per month.

However, extending the loan means paying more interest over the long term. Fix says consumers should carefully read the terms of any refinance agreement. Do the math to see if you’d save money. But even if you’re not, refinancing could still benefit you by enabling you to make your payments.

Sell the vehicle

You could sell your car, use the proceeds to pay off the loan and buy a cheaper vehicle. Some lenders can also arrange for a new buyer to take over the payments on a loan, assuming the buyer qualifies.

“If you have a (car) that no longer works within your budget, then selling the vehicle for one that does is the best route,” says Raj.

Nick Clements, co-founder of MagnifyMoney.com, says it depends on how much equity the person has. Most dealers will allow a buyer to trade in a vehicle with an outstanding loan, but it can be tricky when they’re “upside down.” For example, if a consumer has a vehicle worth $15,000 but owes $18,000 on it, he’ll still have to pay off that $3,000 before trading in the car.

Turn in the keys

Also known as voluntary repossession, this option involves turning over the vehicle to the lender. It could be a solution if you have no equity or no feasible way to keep the car. In some states, however, Weliver says you still must pay the difference between what you owe and what the car sells for at an auction, plus fees.

This decision will heavily impact your credit score, and your credit report will still reflect any balance due. A voluntary repossession should be seen as a last resort.

Car accidents happen all the time. You probably think it won’t happen to you, and this is actually how a lot of people see road accidents. Many people think that if they’re careful, they wouldn’t experience being in an accident. But the thing about being on the road and being involved in a car crash is that it’s not entirely up to you. There are other motorists out there who drive recklessly.

To spread more information regarding the topic, we’ve collected the numbers from some of the most respected sources and made them into easy to understand infographs. We’ll walk you through the breakdown of the stats below.

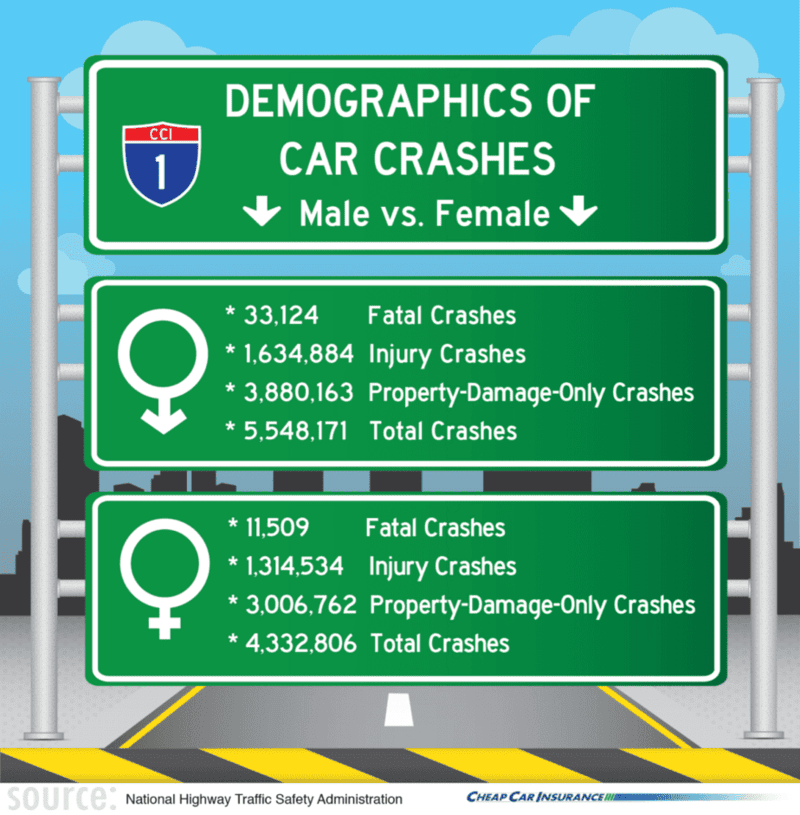

On the infograph above, we can clearly see that males are responsible for more car crashes than females. This does not mean that females are better than males at driving. It may simply be because there are more male drivers, or it may be because males are more likely to participate in risky behavior. Whatever the reason, the important thing to remember is that the numbers on this graph are real. Fatal car crash incidents reach thousands per year and car crashes that injure people and damage property reach millions per year. This means that getting involved in a car accident is not as rare as you think.

Crash Statistics

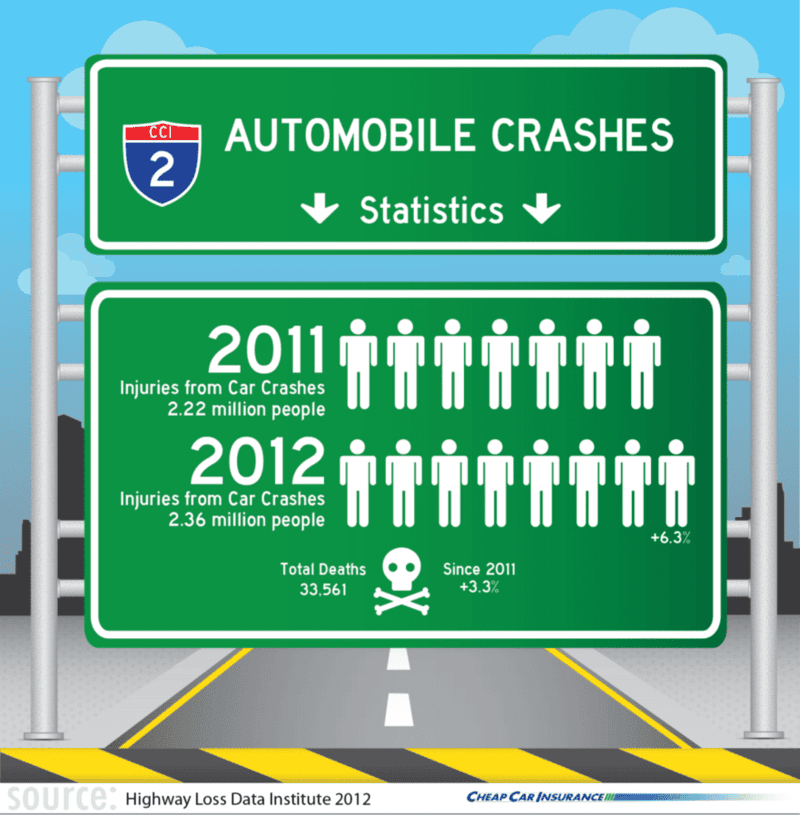

In the data collected from the National Highway Traffic Safety Administration, we can clearly see that the number of deaths and injuries involving vehicular accidents is on the rise. Cars aren’t the only ones responsible for these deaths, damages, and injuries, as motorcycles, bicyclists, and pedestrians also played a part.

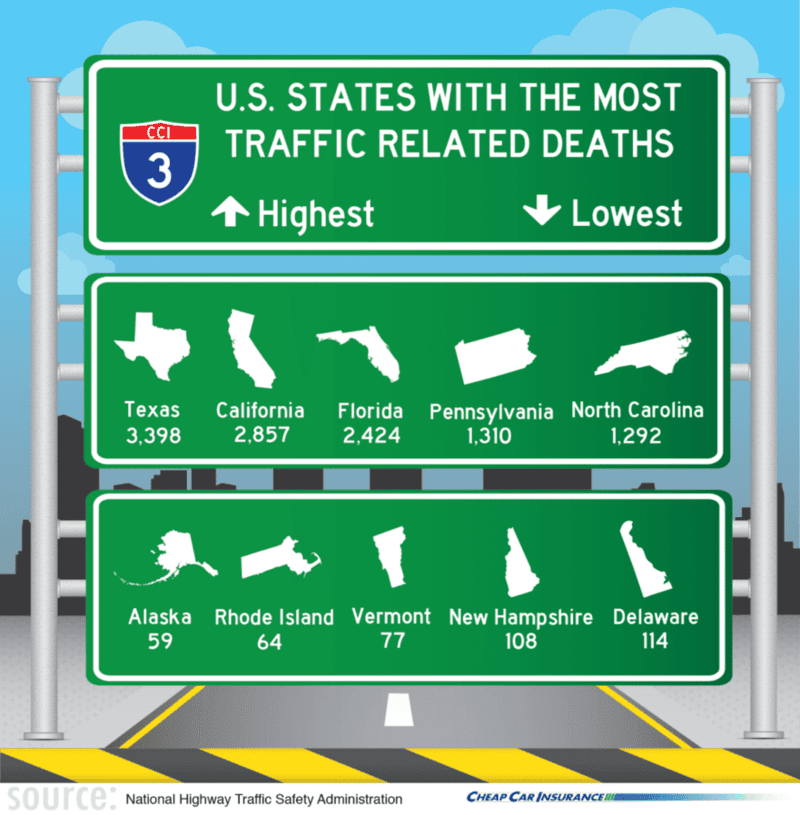

Check out the different states and how they rank when it comes to car accidents.

Laws for Your Driving Protection

Seat Belt Laws

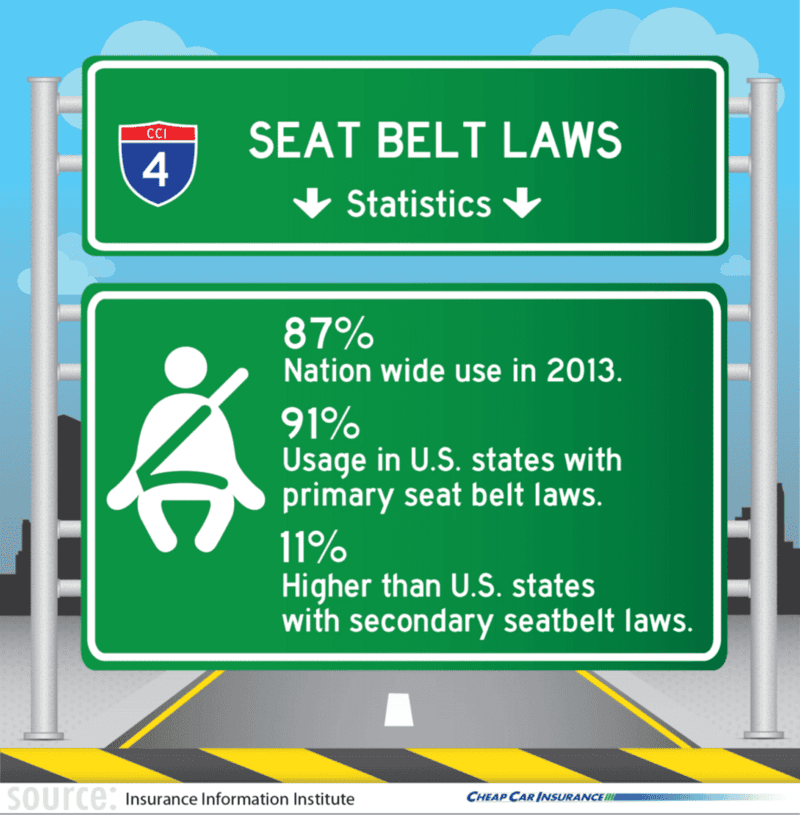

The District of Columbia along with 33 other states have primary seat belt enforcement laws. This means that a police officer can stop a car if the passengers inside the vehicle are not wearing seat belts. The other remaining states have secondary seat belt laws, which mean that the police can issue a seat belt violation only if the driver has broken another traffic rule. Currently, only New Hampshire is without an adult seat belt law. The record for the highest seat belt usage is 87%, which was reached in 2013. States that have implemented a primary seat belt law have an average rate of 91% usage, 11% higher than states who only have secondary seat belt laws.

Drunk Driving Laws

Drunk driving accounted for 10,322 deaths in the U.S. alone in 2012. It has risen by 4.6% from 2011. This upward trend has not always been the case because drunk driving fatalities had been steadily declining since 2003. The trend may be because of the many traffic laws passed since. In D.C., the definition of drunk driving was redefined, setting the limit for drunk driving to 0.08% blood alcohol concentration from the former 0.10%. Many states have also implemented a liquor liability law, which holds bars or businesses serving alcohol accountable for the damages that a drunk driver may cause.

Cellphone Laws

Fourteen states, including the District of Columbia, have already completely banned the use of mobile devices for all drivers while 37 states have restricted cellular phone use for new drivers. As for texting, D.C. plus 44 other states have already prohibited the practice while behind the wheel.

Older Drivers

14% of the population was older than 65 years of age back in 2012. This accounts for around roughly 43.1 million residents. Despite their small number, the drivers from this age group accounted for 17% of all car accidents in the same year. For this reason, additional laws have been passed restricting the licenses of older motorists. This could mean being allowed to drive but only during the day, or a restriction to drive on some major freeways. Needless to say, this depends on every driver’s ability. Some younger drivers may even get a restriction if they have a medical condition that could affect their ability to drive.

Young Driver Laws

Unsurprisingly, drivers who are young account for a large number of vehicular accidents. For this reason, some states have adopted laws in which young drivers aren’t allowed to drink even small amounts of alcohol. Almost all States including the District of Columbia have also implemented a Graduated Drivers License program for 15- to 18-year olds, where people who are learning how to drive go through a more rigorous and longer process before getting a driver’s license. According to the National Highway Traffic Safety Administration (NHTSA), this program involves 3 stages. Initially, the student driver obtains a learner’s permit and approval would depend on the results of a vision test, a road knowledge test, driving accompanied by a licensed adult, seatbelt use by everyone in the car, a zero BAC level, and six months without a crash or a conviction for traffic violations. The second stage includes a behind-the-wheel road test, advanced driver education, driving accompanied by an adult at night, and 12 consecutive months without a crash or traffic violation conviction. After this, they can apply for a full and unrestricted driver’s license. The only exception to this is New Hampshire, as they do not issue learner’s permits.

Different states require different durations before issuing a driver’s license to learner’s permit holders. In most cases, 6 months is the required duration. Colorado, Florida, Georgia, Iowa, Kansas, Mississippi, North Carolina, North Dakota and Vermont, however, require a 12-month learner’s permit provisional period. Virginia requires 9 months, while Wyoming only requires a provisional period of 10 days.

In addition, restrictions on night driving for teens have been implemented in all states except Vermont. Excluding Florida, Iowa, Mississippi, North Dakota, and South Dakota, all the other states have also created a regulation restricting the number of teen passengers allowed in a single vehicle when the driver is also a teenager. This is because according to the Children’s Hospital of Philadelphia and State Farm, teens have a greater risk of getting involved in a car crash if other teens are in the vehicle as well.

Driverless Cars

Nevada was the first state that approved driverless or self-driving cars on the road in May 2012. California, Florida, Michigan, and the District of Columbia have since passed similar laws and many other states are considering doing the same.

Aggressive Driving

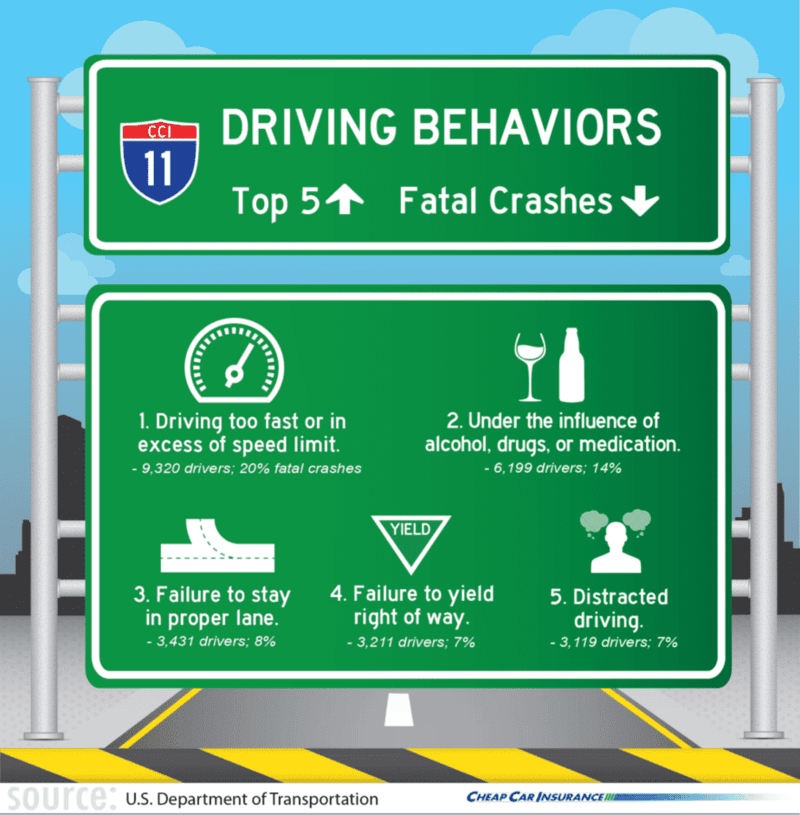

According to the National Highway Traffic Safety Administration (NHTSA), aggressive driving is a “major factor” in traffic accidents, “playing a role not just in well-publicized incidents of road rage, but in a large number of fatal highway collisions each year.” NHTSA defines aggressive driving as “an individual commits a combination of moving traffic offenses so as to endanger other persons or property.” Even though the definition of “aggressive driving” still remains fluid to this day, one of the main factors that constitute accidents that would fall on aggressive driving is speeding.

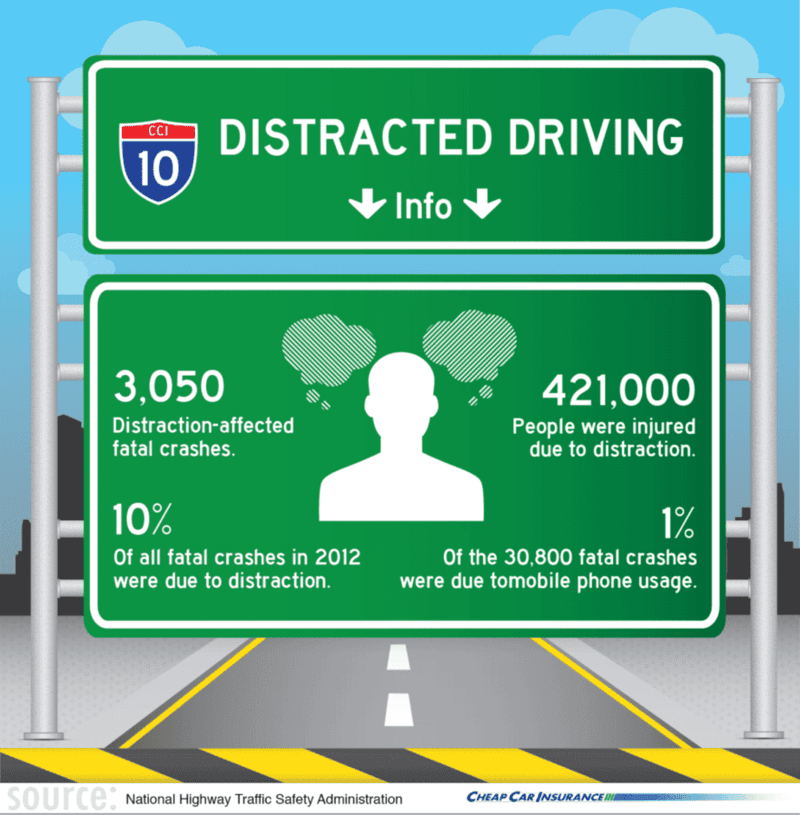

Distracted Driving

The definition of “distracted driving” according to NHTSA is “activities that take a driver’s attention off the road, including talking or texting on cellphones, eating, conversing with passengers and other distractions.” In 2010, NHTSA updated the way they evaluated distracted driving through a more specific measure called “distracted-affected crashes,” this focuses more on the actual distractions that are most likely to impact accident involvement like using mobile devices and being distracted by a passenger or other external events.

Driving Behaviors Reported For Fatal Crashes

Theft Statistics

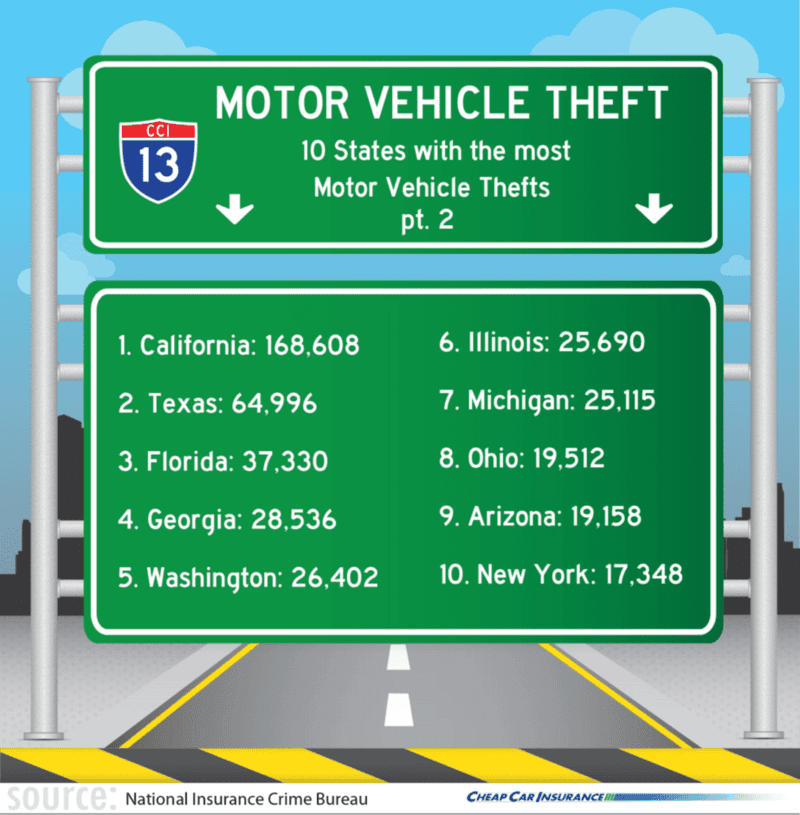

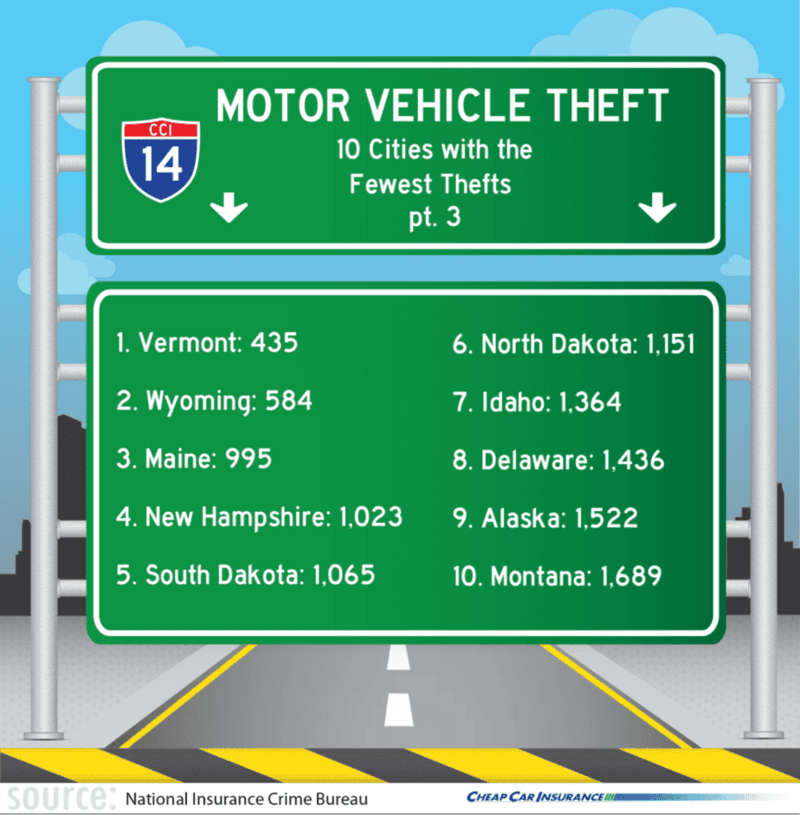

No matter how many laws are passed to prevent accidents that would harm you and your vehicle, accidents happen. Worse, theft happens. In 2011, around 230 vehicles were stolen for every 100,000 according to the National Insurance Crime Bureau. This amounts to more than $4.3 billion in losses due to vehicle theft. The average price per vehicle theft was $6,089.

Top 10 Cities With The Highest Motor Vehicle Theft Rates

Top 10 States With The Most Motor Vehicle Thefts

Top 10 Cities With The Fewest Motor Vehicle Thefts

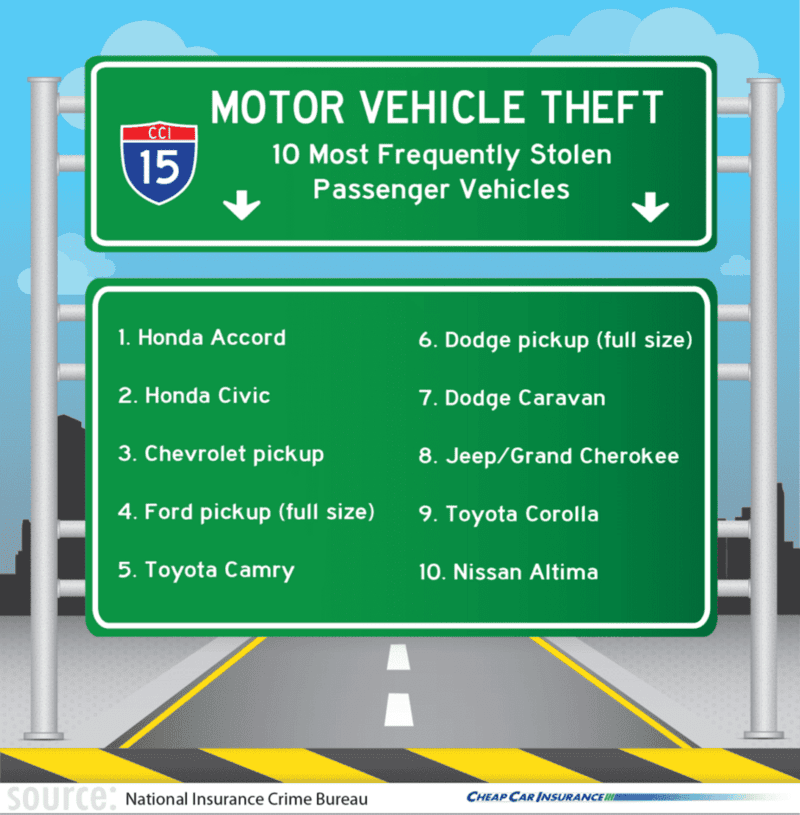

Top 10 Cities Most Frequently Stolen Passenger Vehicles

Uninsured Motorists

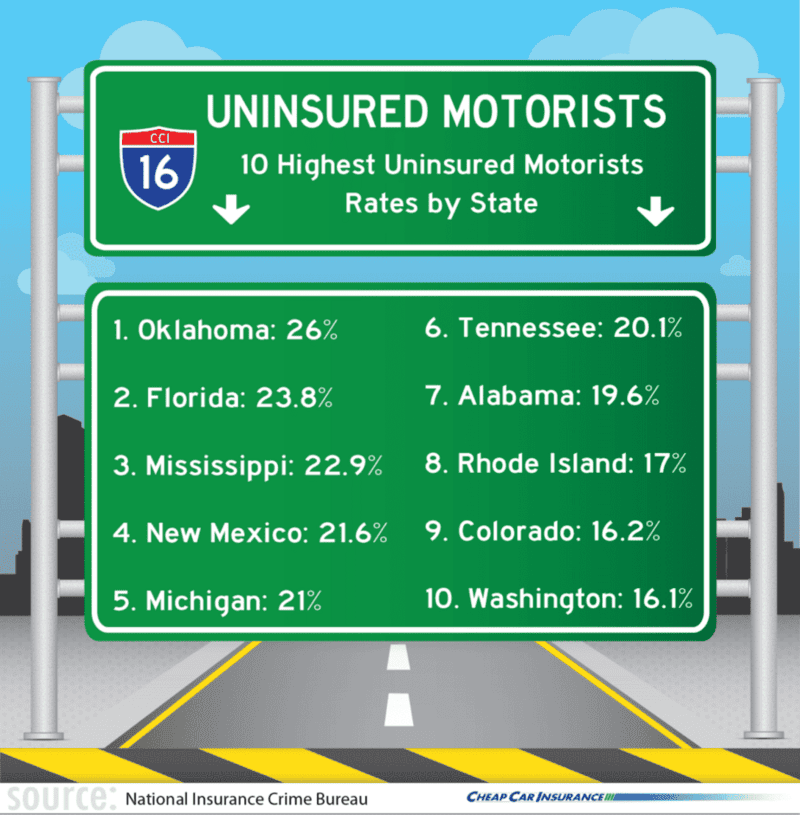

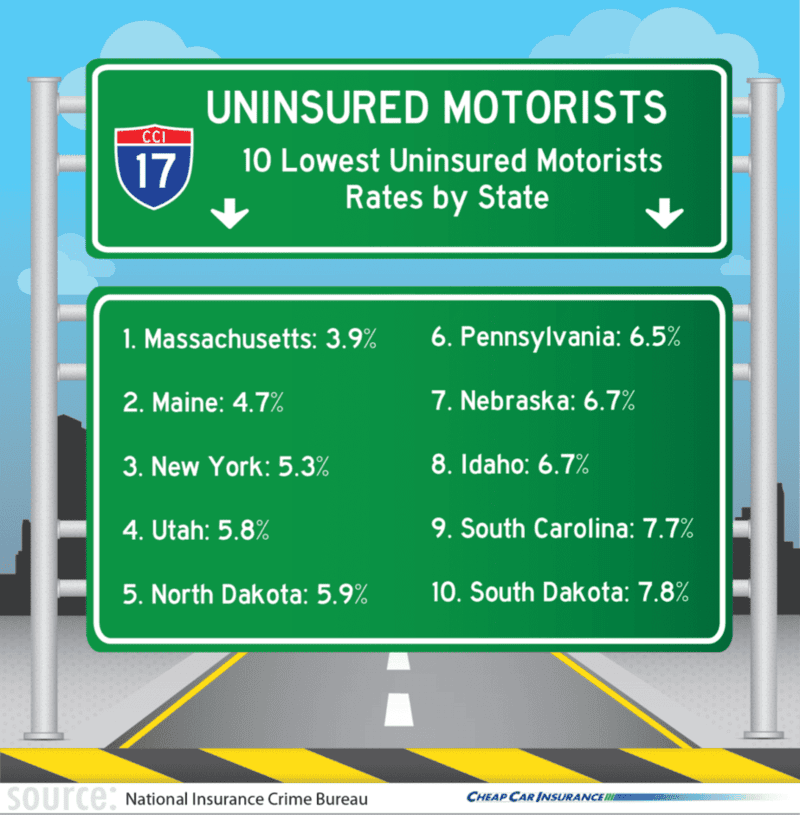

Despite these glaring numbers on car fatalities, not all motorists are insured. In 2012, about one in every eight or 12.6 percent of drivers were uninsured. Though this percentage has declined in recent years, some states still have an alarming number of motorists who are uninsured. Oklahoma had the highest rate of uninsured drivers at 26%. Massachusetts, on the other hand, had the lowest incidence of uninsured motorists at only 4%, according to a 2014 study by Insurance Research Council.

Forty-nine states along with the District of Columbia oblige motorists to have some form of auto liability insurance. New Hampshire is the only state that does not necessitate the purchase of insurance although they have a financial responsibility requirement. This mandate requires drivers to prove that they have the financial capability of paying for damages in case they meet an accident. According to the Insurance Information Institute, some states including Texas, Nevada, Oklahoma, Wyoming and California already have online auto insurance verification systems to detect uninsured drivers.

Top 10 Highest Uninsured Motorists By State

Top 10 Lowest Uninsured Motorists By State

General Property/Casualty Statistics

In 2013, the U.S. insurance industry’s net premiums alone amounted to $1 trillion, with property/casualty insurers accounting for 46% of recorded premiums. This was calculated after deducting certain risks that are transferred to other insurers, according to SNL Financial. Out of the leading 10 global insurance companies in 2013, two were U.S. based, namely Berkshire Hathaway, which took the number one spot and United Health Group at number five. From 2004 to 2013 alone, the property and casualty net premiums written increased by 13%.

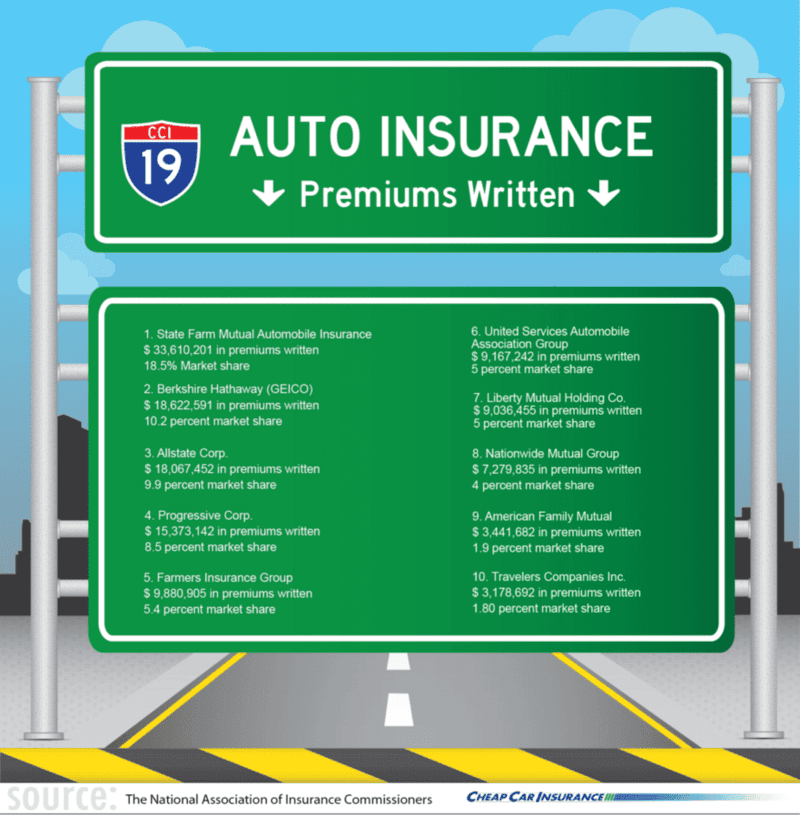

Auto Insurance Premiums Written

In 2011, the total private passenger auto insurance premiums written amounted to $163.3 million, while $168 million and $174.8 million worth of insurance premiums were written in 2012 and 2013 respectively.

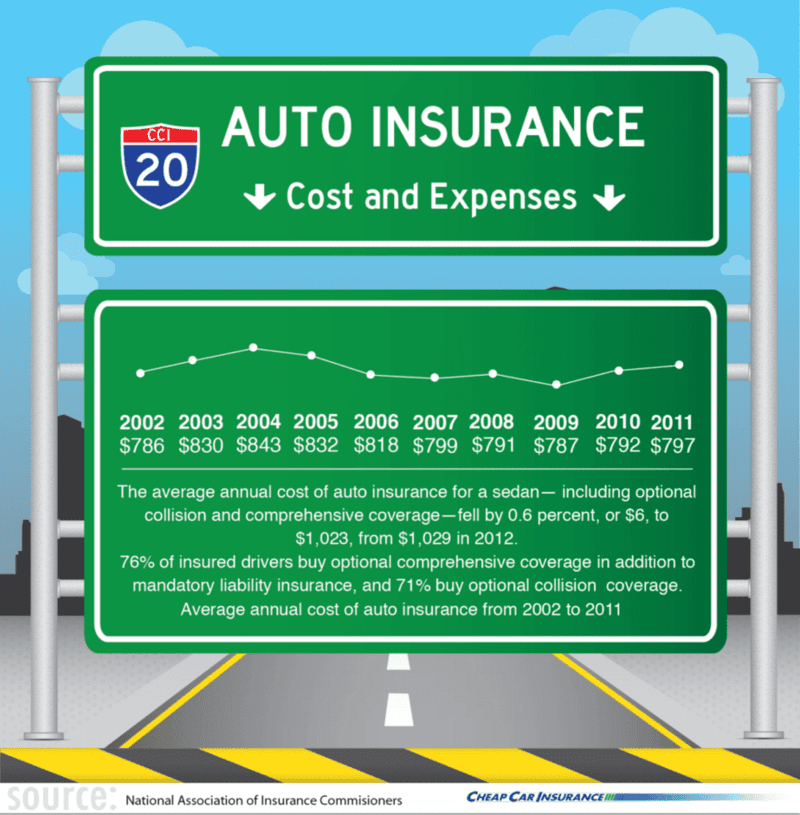

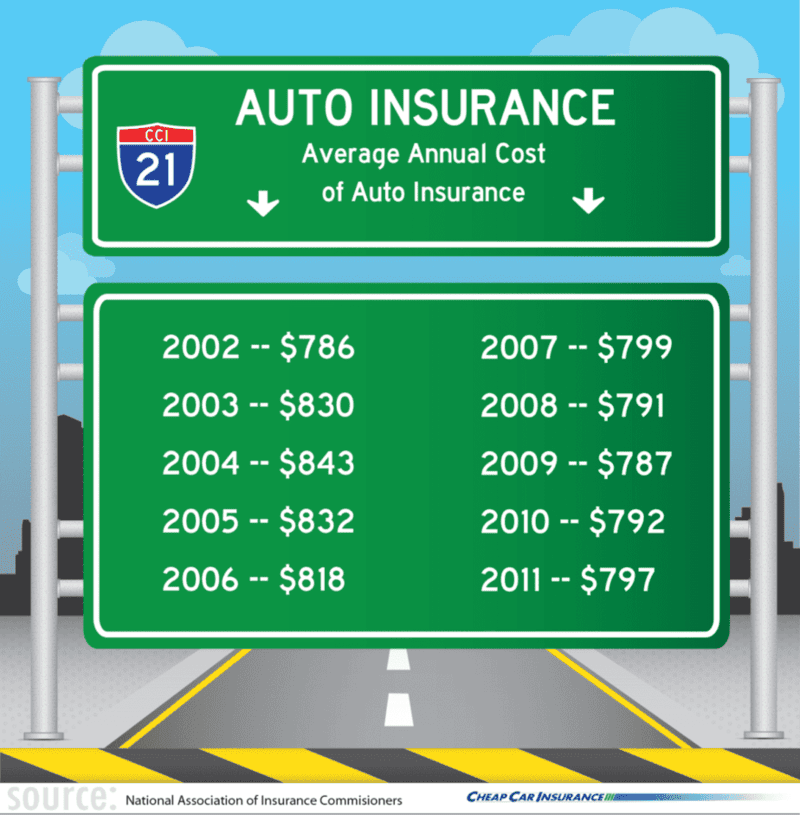

Auto Insurance Costs and Expenses

A study by AAA’s 2014 Young Driving Costs revealed that the average cost to own, operate, and maintain a sedan was $8,876 in 2013. This has decreased by 2.7% (roughly $246) from the year before. According to the results of the study, “The cost reflects a relatively large decrease in fuel costs and lower tire, depreciation, and insurance costs.”

As for the average yearly cost of auto insurance for a sedan, it fell by 0.6% from 2012. This includes collision and comprehensive coverage. According to the National Association of Insurance Commissioners, 76% of drivers pay for the additional comprehensive coverage on top of the required mandatory liability insurance, while 71% opt for collision coverage.

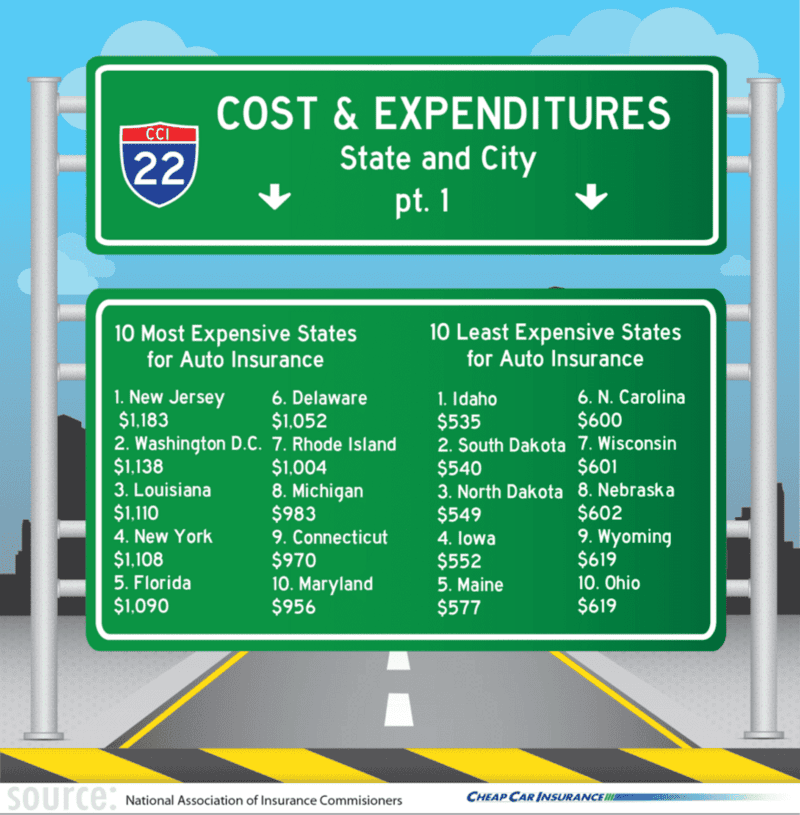

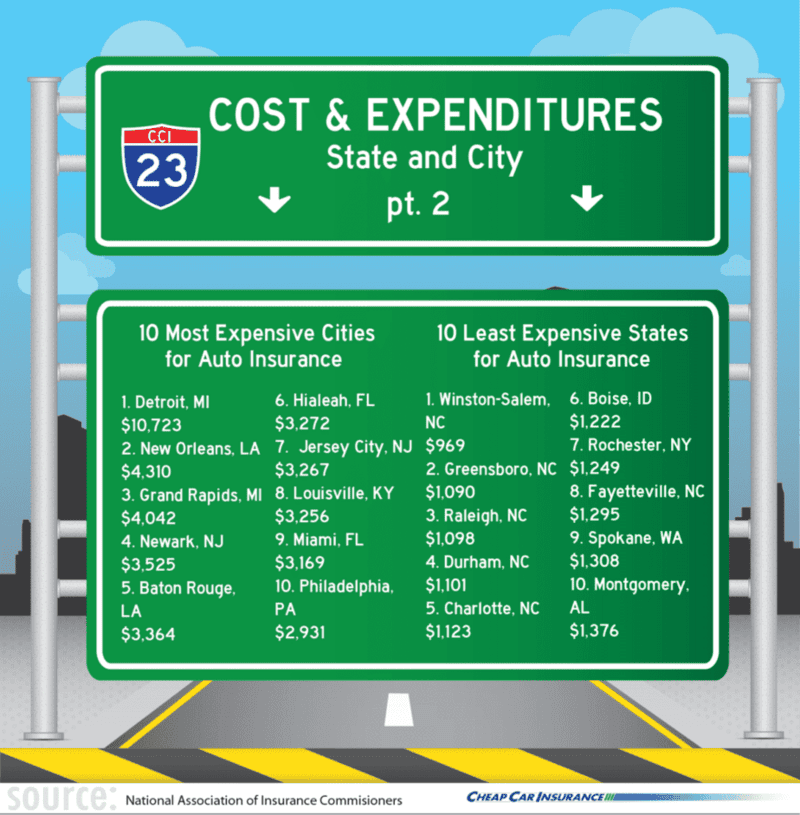

Costs And Expenditures By State And City

According to the National Association of Insurance Commissioners, people are more likely to buy brand new cars in states where the economy is doing well. These brand new car owners are also more inclined to buy physical damage coverage.

Location is another factor when it comes to premiums. Places that are more populated and with higher per capita income tend to also be high-premium states since the wages in urbanized areas are also higher. The costliest city for auto insurance is Detroit where prices are almost double the amount as compared to the second priciest city, New Orleans. Six of the cities with the cheapest car insurance are in North Carolina with Winston-Salem as the cheapest.

In 2013 alone, the total losses incurred by private passenger auto insurance reached $109.6 billion. According to ISO, less than 1% of those with liability insurance had physical injury claims and only 3.6% had property damage liability claims.

High Risk Markets

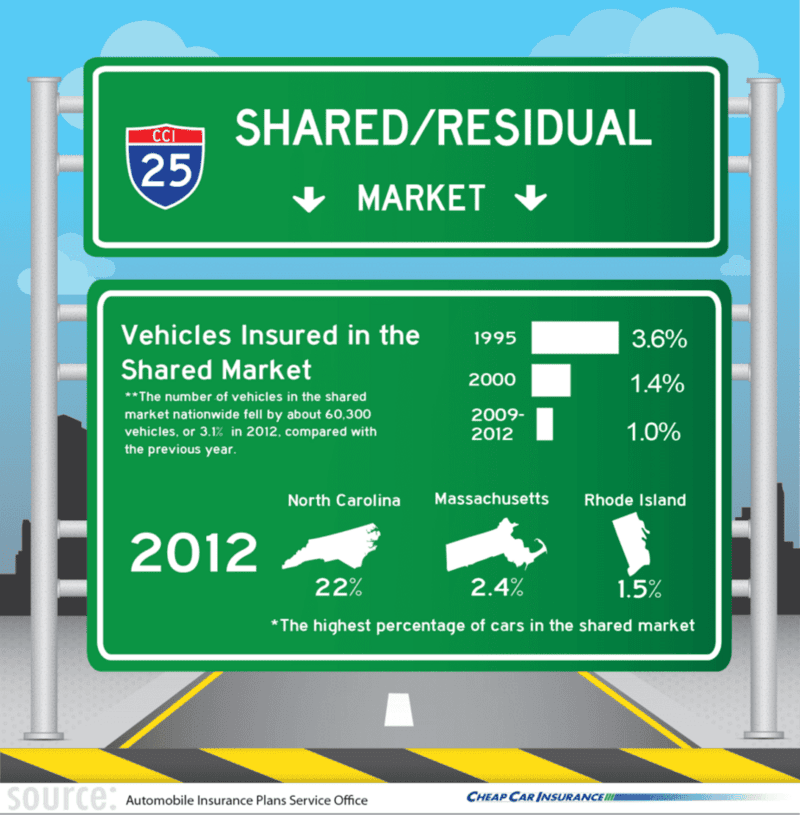

The Shared/Residual Market

All states in the U.S. have put up systems that help give car insurance for those who can’t afford it. They call them assigned risk plans. The insurance industry refers to these as the shared, or residual, market. The percentage of vehicles in the shared market is dropping, however, according to the Insurance Information Institute. One of the reasons why this is happening is because of the decline in the “nonstandard” sector of the voluntary market. This is for drivers with poor driving records or those who drive specialized vehicles.

Auto Insurance Laws

No Fault

The no-fault system is for lowering the cost of car insurance by taking small claims out of the court. In a state with a no-fault law, every insurance company reimburses its own policyholders for minor damages irrespective of whose fault the accident was. This is known as personal injury protection (PIP). PIP coverage is compulsory in no-fault states although the benefits vary depending on which state you’re in. The no-fault states include Florida, Hawaii, Kansas, Kentucky, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Dakota, Pennsylvania, Puerto Rico, and Utah.

Drivers who reside in no-fault states may sue if there are bodily injuries sustained as long as the case meets certain conditions. These conditions are referred to as tort liability threshold. It may be expressed in verbal terms including death or disfigurement or in monetary amounts of medical bills.

“Choice” No Fault

For “choice” no-fault states, motorists can choose out of two options: a no-fault auto policy or a traditional tort liability policy.

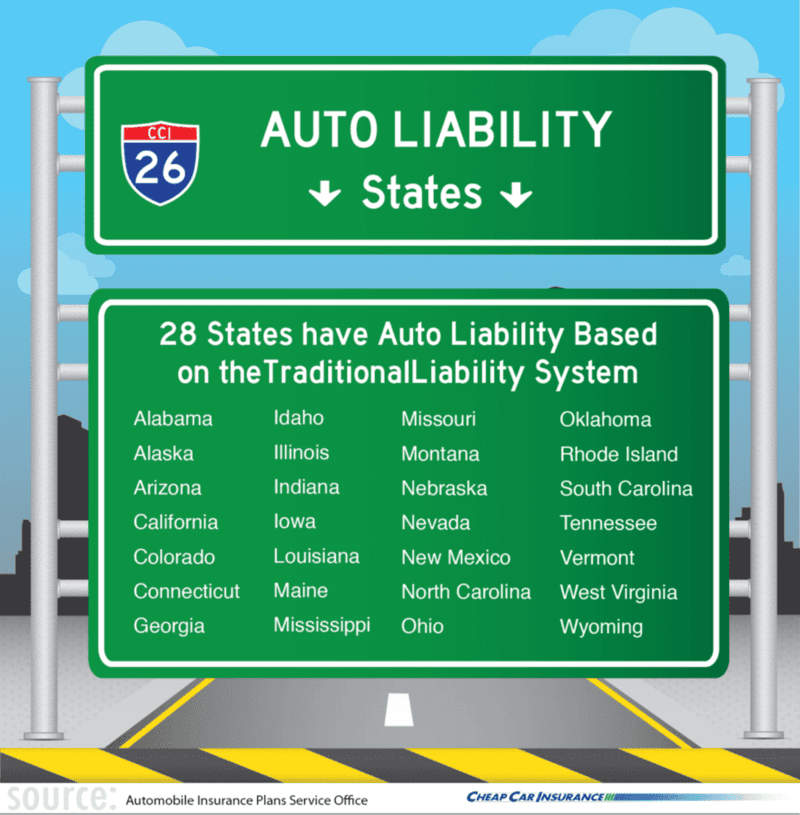

Tort Liability

There are no limitations on lawsuits in customary tort liability states. For states with this law, the passenger injured can sue the driver at-fault for any bodily harm, inconvenience, and expenses that he or she sustained during the accident.

Add-on

For states with the add-on policy, drivers can obtain medical coverage and other coverages from their insurance company. The only difference they have in no-fault states is that there are no restrictions on lawsuits. “Add-on” is the term used because these benefits are added to the customary tort liability system. In add-on states, first-party coverage may not be required and the benefits may be inferior to that of true no-fault states. The “add on” no fault states include Arkansas, Delaware, Washington D.C., Maryland, New Hampshire, Oregon, South Dakota, Texas, Virginia, Washington, and Wisconsin.

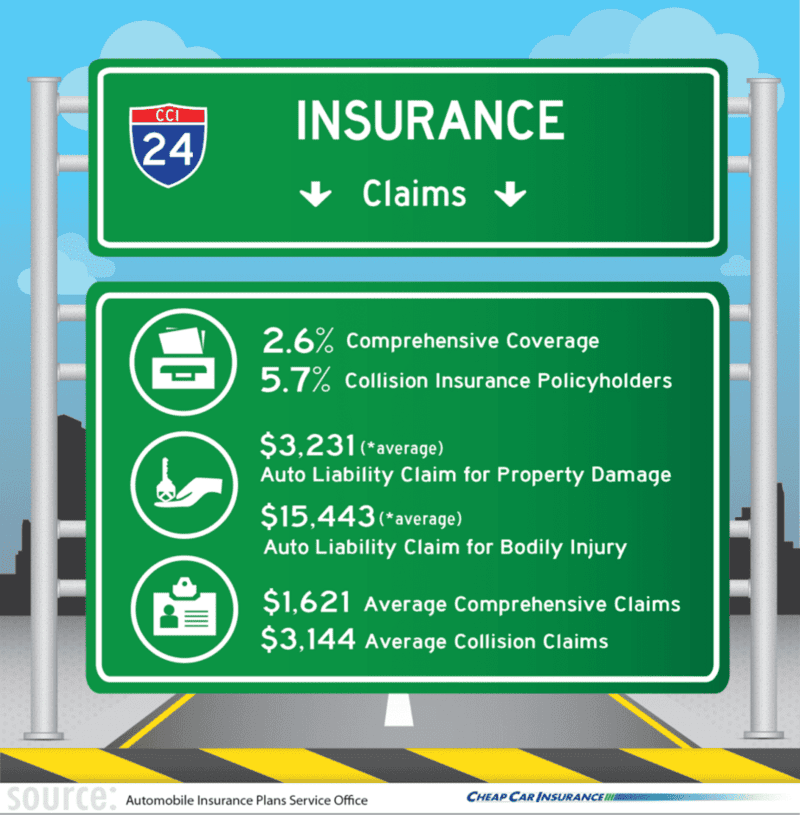

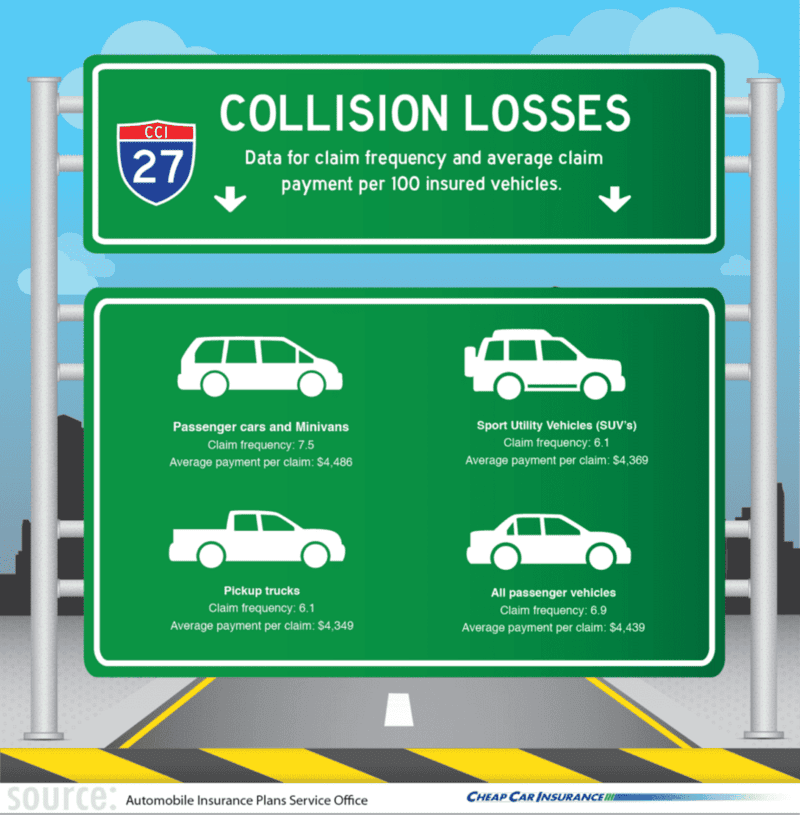

Collision Losses

Take a look at the 2012 data for claim frequency and average claim payment per 100 insured vehicles. (Source: Highway Loss Data Institute)

Conclusion

Paying for car insurance may seem expensive now but getting in an accident without insurance would cost more. Finding the best policy may not be easy since there are a lot of insurance companies in the market, but if you do your research and know what kind of coverage you want, the process is much smoother. Look for an insurance company who can provide personalized coverage instead. This may be better for your budget since you don’t have to pay for unnecessary fees.

A vehicle means more than just a machine to most. It can be one’s symbol of success, the reward for one’s continuous hard work, or even a representation of love for some who received their car as a sentimental gift. Have your car insured and protect not just your vehicle, but also your loved ones as well.

By Aaron Crowe

Being in a car accident is traumatic by itself. Dealing with the aftermath — such as seeking treatment for your injuries, filing an insurance claim and getting legal advice — can add to the stress.

Being in a car accident is traumatic by itself. Dealing with the aftermath — such as seeking treatment for your injuries, filing an insurance claim and getting legal advice — can add to the stress.

At a time when you may not know what to do next, it can be difficult to decide if you need a personal injury attorney.

If your car suffers damage in an accident but you don’t, your insurance company should work on your behalf to get you reimbursed, and you probably won’t need a lawyer. But if you’re injured in a car accident, an early consultation with a lawyer may be the right move. An attorney could help you win a larger settlement that goes toward your medical bills following an accident.

Here are seven tips to help you find a personal injury attorney after you’ve been hurt in a car accident.

- Act fast.

The longer you wait to contact an attorney, the harder it gets to take a case to trial. Much of your initial decision may rest on how helpful the other driver is.

If the other driver in your accident is immediately cooperative, you might not need to hire an attorney. But if that person is unhelpful, you may need legal help to get all relevant information.

Many lawyers offer free initial consultations in these types of cases, and consumers should avoid lawyers who don’t, says Andrew Vines, a personal injury attorney in Little Rock, Arkansas.

“In that consultation, the lawyer can discuss your case and let you know whether you have a valid claim that can and should be pursued,” Vines says.

- Do your research.

You may see late-night TV commercials or an ad on the side of a bus for attorneys who claim to collect large payments for people injured in car crashes. Such advertising doesn’t necessarily mean an attorney is good or bad at their job, but their claims should be checked out.

You can research an attorney’s record online at your state bar association or through an online directory at the American Bar Association. Your local or state bar association may also have a lawyer referral service.

Friends and family can also offer referrals, or ask an attorney you’ve worked with in the past.

- Find a specialist.

If you have a specific type of injury, such as a broken back, then a law firm that specializes in your injury can be helpful.

“If you have sensitive injuries or a unique situation, make sure the attorney has been involved in a case like yours before,” says Hamilton Lindley, a personal injury lawyer in Waco, Texas. .

At the very least, find a lawyer who specializes in vehicle accidents, says Lawrence J. Buckfire, a personal injury lawyer in Michigan.

“There are a number of complicated insurance issues involved in auto accident cases, and you need an attorney who has experience and extensive knowledge on those issues,” Buckfire says.

- Interview lawyers.

Talk with your attorney to determine if his skills and experience match your needs, and ask for professional references.

To find the best lawyer, Buckfire recommends asking these questions:

- How long have you been handling car accident cases?

- What percentage of your practice is devoted to car accident cases?

- Which attorney in your office will be handling my case?

- Has that attorney won substantial verdicts in car accident cases?

“Most importantly, you need to feel comfortable with the attorney you work with because the process can take a long time,” Buckfire says.

- Seek trial experience.

Ask how many cases your attorney takes to trial each year versus making settlements.

“While the goal of most cases should be to settle them for a fair amount without the need to go to court, a lawyer with experience in taking cases to court can often do a better job of recovering fair value for your case than a lawyer without trial experience,” Vines says.

A lawyer who has taken cases to trial knows how juries value cases, Vines says. That lawyer would know how to negotiate a settlement.

- Avoid promises.

In the initial consultation, you want a lawyer who will be straightforward with you about the litigation process and pros and cons of pursuing a case, Vines says. But don’t listen to promises that you’ll be rich or that you’ll even win the case, he warns.

Compensation or full financial recovery in cases is never guaranteed.

“Any lawyer who makes a promise about what you can recover should be avoided,” Vines adds.

- Know your costs.

Your auto insurance company won’t pay for you to hire an attorney to file a lawsuit after an injury.

Most personal injury attorneys work on a contingency basis, meaning they don’t get paid unless the client wins. Payment varies by state, but in general lawyers collect one-third of a personal injury settlement or judgment. You shouldn’t pay anything if the case is lost.

Some lawyers may ask for upfront costs, regardless if they lose the case.

By Aaron Crowe

Driving through a parking lot can feel almost as stressful as driving on a busy freeway. With cars backing out of parking spaces and people walking through with their attention on their phones, even the slowest driver needs to be extra wary.

Driving through a parking lot can feel almost as stressful as driving on a busy freeway. With cars backing out of parking spaces and people walking through with their attention on their phones, even the slowest driver needs to be extra wary.

Parking lot accidents are common, with about 20 percent of all auto accidents taking place in parking lots. Serious damage to your car is unlikely, though you could develop physical injuries such as whiplash days later.

Since the damage is often minor, both drivers may be inclined to not report it to police or their insurance companies. That can be a mistake for many reasons. Here are some steps to take after you’ve been in a parking lot accident:

- Everyone OK?

Injuries from parking lot accidents are uncommon, but the first thing to do is check that you and the other driver aren’t injured, says Will Smith, a personal injury attorney in Atlanta who has represented clients involved in parking lot crashes.

“Because they’re going so slow a lot of times, they’re not injured,” Smith says. “But it happens.”

If you’ve been injured or feel pain, you should seek prompt treatment. Call an ambulance if needed. Your adrenaline may prevent you from feeling symptoms of certain injuries such as whiplash, Smith says, so it could be worthwhile to go to your medical provider and get checked out.

“Seemingly minor accidents can turn into major health issues,” says Cade Parian, a personal injury attorney in Atlanta.

- Don’t argue

Anger and frustration are common after an accident, but don’t argue with the other driver over whose fault it is. It can lead to a physical fight, which no one wants, or at the least to someone saying something they’ll regret — such as being at fault.

- Gather information

Just as you would in any other auto accident, you’ll need to exchange names, addresses, phone numbers and insurance information after a parking lot accident — even if you consider it a small accident that won’t need repairs.

It may be too early to tell if your car has been damaged. There may be internal damage that isn’t apparent yet, or you may be too shaken up to notice it.

Having this information will help your insurance adjuster work on your behalf. Either call your insurance company from the scene or wait until you get home.

You should also get contact information from witnesses, if there are any, and take photos with your phone of the scene and the other car, including its license plate, Parian says.

- Call the police

Parking lot accidents generally occur on private property, so police may not issue a citation to the offending driver, Smith says. Police may not even respond to such an accident unless someone is injured, and they may not issue a police report.

Still, it’s worthwhile to call police after a parking lot accident, because they may come out and file a report, Smith says. A police report can be a tremendous help to your insurance company.

In Georgia, drivers can ask police to prepare a “Georgia Uniform Motor Vehicle Private Property Accident Report,” Smith says. The document will record pertinent information about the accident and will be useful later to insurance companies.

Even if neither car is damaged and both parties are uninjured, filing a police report can help if either side claims injuries months later.

“Your insurance company is going to rely a lot on what that responding officer reports,” Parian says.

- Call your insurer

We mentioned this earlier, but after these initial steps have been taken, it’s time to call your insurer and let them know you’ve been involved in an accident — no matter how small.

Almost all insurance policies require that the insured report accidents. It’s part of your contract with your insurer to cooperate with them. Without it, you could lose coverage.

If you’re at fault in the accident, you’ll have to pay your deductible and you’ll be assigned points, which will cause your insurance rates to rise.

However, a minor accident in a parking lot may be one of the few times when it’s worthwhile not to file a claim. You could pay for the damage yourself if the repairs cost less than the deductible.

Backing up out of a parking space is the most common parking lot accident, Smith says. If you backed your car into another car, you’ll probably be found at fault.

Some parking lot accidents could come down to your word against the other driver, when insurance companies could split the fault in half. Each person would pay their deductible and no points would be assigned.

- Contact an attorney